Markets Confusing? Ask Edgen Search.

Instant answers, zero BS, and trading decisions your future self will thank you for.

Try Search Now

A constructive outlook on Bio Protocol’s strategy, product, token model, catalysts, and valuation, leaning positive while noting key execution levers. For Bio Protocol Guide, click here

TL;DR

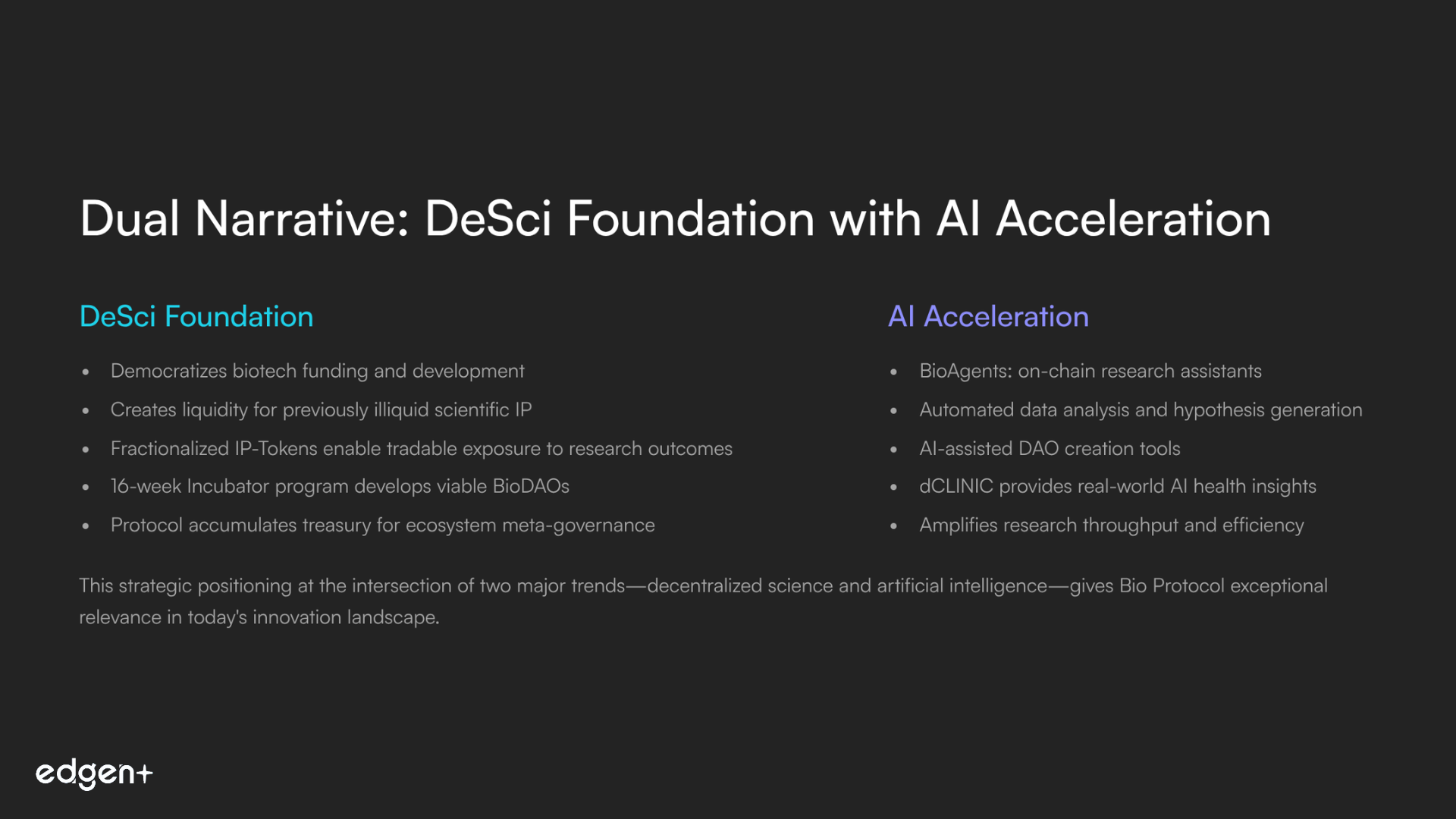

- Positioning: Authentic DeSci leader that also taps the AI super-trend (BioAgents, AI-DAO tools).

- Product: End-to-end stack, curation > launch > liquidity > meta-governance > secondary markets, plus IP-Tokens and a coming BioAgents layer.

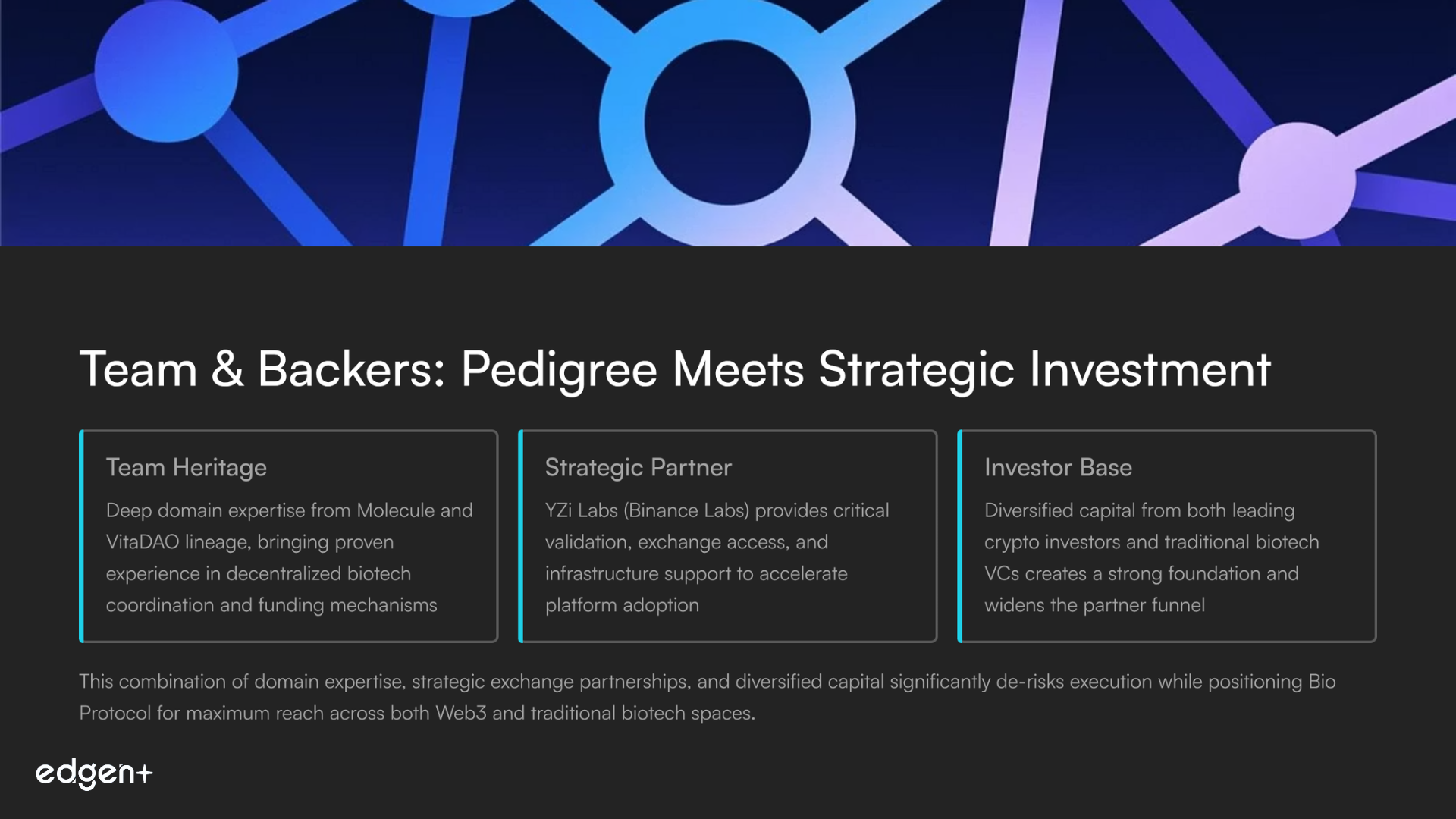

- Team/Backers: Deep domain team (Molecule/VitaDAO pedigree) + YZi Labs (Binance Labs) and top crypto/biotech investors.

- Economics: Clear demand via staking > BioXP > Ignition Sales; emissions are sizable, watch % of unlocked BIO staked and any burn/liquidity recycling.

- Catalysts: Bio Markets, first Ignition Sales, dCLINIC v1.0, Percepta readout, AI-DAO tools; long-tail upside from enterprise IP tokenization.

What is Bio Protocol

Bio Protocol is a financial + operational layer for decentralized biotech. BIO stakers (veBIO) curate new BioDAOs; selected projects raise via Ignition Sales; the protocol seeds liquidity, distributes milestone rewards, and accumulates a treasury of ecosystem tokens for meta-governance. A dedicated Incubator (16 weeks) helps teams become viable BioDAOs, while IP-Tokens (IPTs) fractionalize scientific IP/royalties for tradable exposure.

V2 extends into Bio Markets (secondary trading with fee capture) and AI BioAgents, on-chain research assistants slated to automate data analysis and hypothesis generation—ultimately enabling AI-assisted DAO creation. Deployed on Ethereum & Base, with Solana expansion planned, Bio Protocol aims to become the default launch venue and exchange layer for on-chain science.

I. Foundational & Strategic

Vision fit. Dual-narrative alignment (DeSci + AI) gives Bio Protocol outsized relevance: it funds and accelerates research while making IP liquid.

Product moat. Five-ops engine + IPT design + Launchpad/Markets create sticky network effects; AI BioAgents can amplify throughput.

Market. Accesses budgets from biotech R&D/clinical trials and Web3 infra; even small penetration yields meaningful TVL/fees.

Team/Backers. Molecule/VitaDAO lineage and YZi Labs validation de-risk execution and listings; crypto + biotech investors widen the partner funnel.

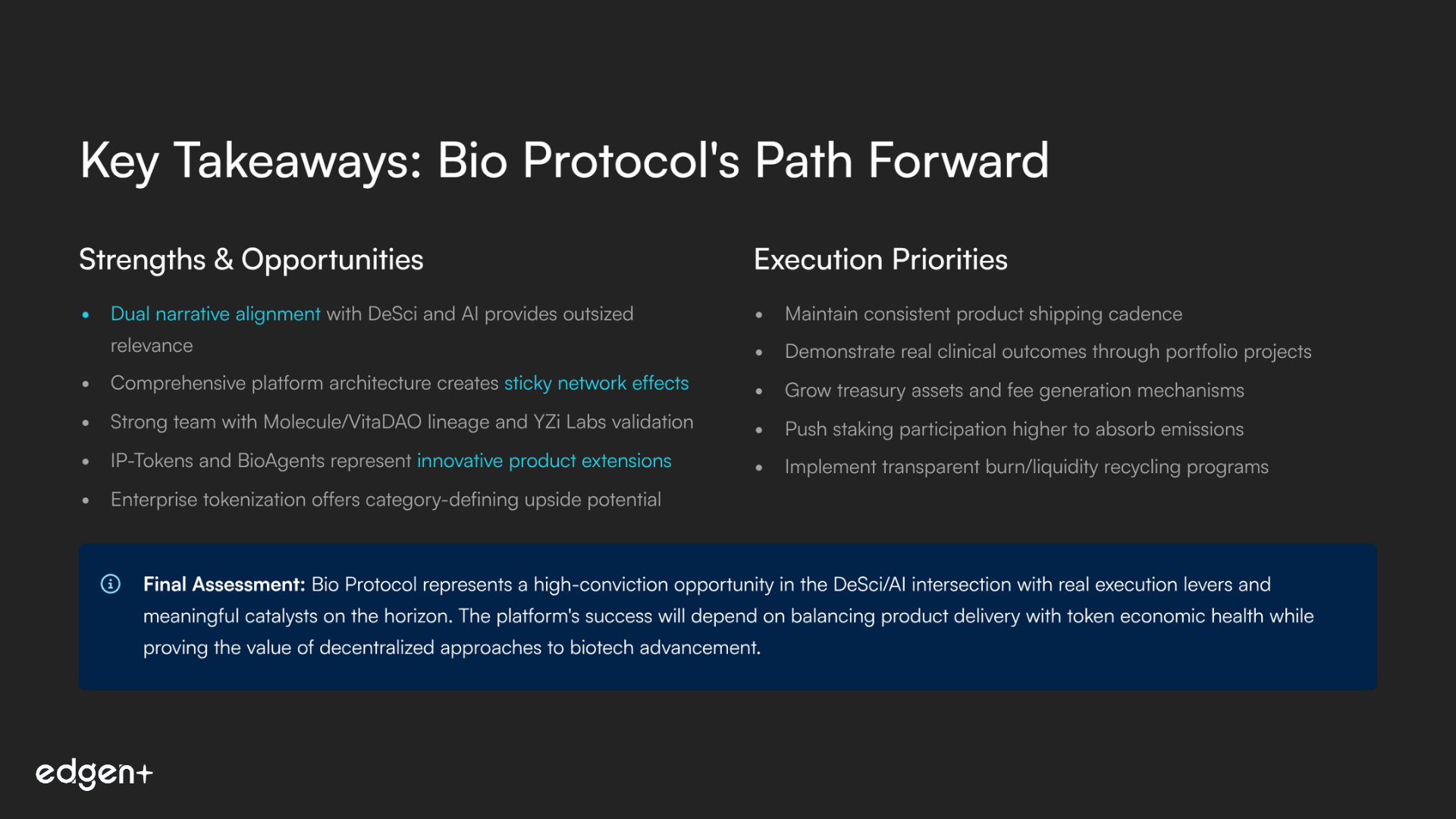

Foundational take: Strong platform architecture and credible team in the right narratives at the right time.

II. Tokenomics & Value Accrual (What to watch)

- Supply: Fixed max (3.32B) but multi-year vesting (contributors/investors/community) = persistent emissions; key periods begin Nov ’25 (linear).

- Demand: Staking → veBIO/BioXP → Launchpad access has traction; BIO pairs in new pools deepen structural demand.

- Treasury/Fees: 6.9% token allocation from launches + share of secondary trading fees; value returns via liquidity recycling / potential burns (visibility important).

- Health gauges: % of unlocked BIO staked, Launchpad cadence/oversubscription, Bio Markets volume/fees, treasury NAV, and any on-chain burn proof.

III. Catalysts & Opportunities

Near term (≤1 month)

- First Ignition Sale (AI agent): validates V2 launch mechanics and BioXP loop.

- Bio Markets + BioAgents surface: enables IPT/BioAgent trading and fee capture.

- dCLINIC v1.0: showcases real-world AI health insights; strengthens “RWA biotech” narrative.

Mid term (1–3 months)

- Percepta Phase 2 readout: binary narrative mover; success validates DeSci curation + royalty IPTs.

- Team/advisor linear vesting begins (Nov ’25): sustained supply headwind; absorption depends on staking and product traction.

- AI DAO-creation tools: lowers launch friction; could accelerate the BioDAO pipeline.

Long term (6+ months)

- Enterprise IP tokenization pilots (e.g., Pfizer): category-defining upside if formalized.

- AI-managed BioDAOs: end-state autonomy; powerful, longer-dated optionality.

IV. Valuation Scenarios

Scenario | FDV / MC (USD) | Why it happens |

Bull | $2.3B – $3.3B | Positive clinical data + smooth Markets/Agents launch; staking >15% of unlocked supply; treasury/fees scale. |

Base | $700M – $1.2B | Strong delivery, but risk-off tape; emissions cap multiple; steady but not explosive fee growth. |

Bear | $300M – $500M | Delays/weak readouts; Markets under-used; staking lags emissions; narrative premium fades. |

Ranges are illustrative; not financial advice.

Final Take

Bio Protocol is a credible platform-of-platforms for on-chain science with a timely AI extension. The upside path is clear: keep shipping (Markets, Agents, AI-DAO tools), prove real outcomes (Percepta, future trials), and grow the treasury/fees while pushing staking higher to absorb emissions. If execution keeps pace with the roadmap and clinical catalysts break favorably, the upper valuation bands come into view; if not, emissions become the gravity. Overall: a high-conviction DeSci/AI bet with real levers—and real execution demands.

Recommend

.ee9b0bcf9fc168ac.png)

.32b68d3b2129e802.png)