Bittensor is a peer-to-peer network creating an 'Internet of AI' where intelligence is a tradable commodity, democratizing access and development. For a shortened version of the guide, click here.

TL;DR

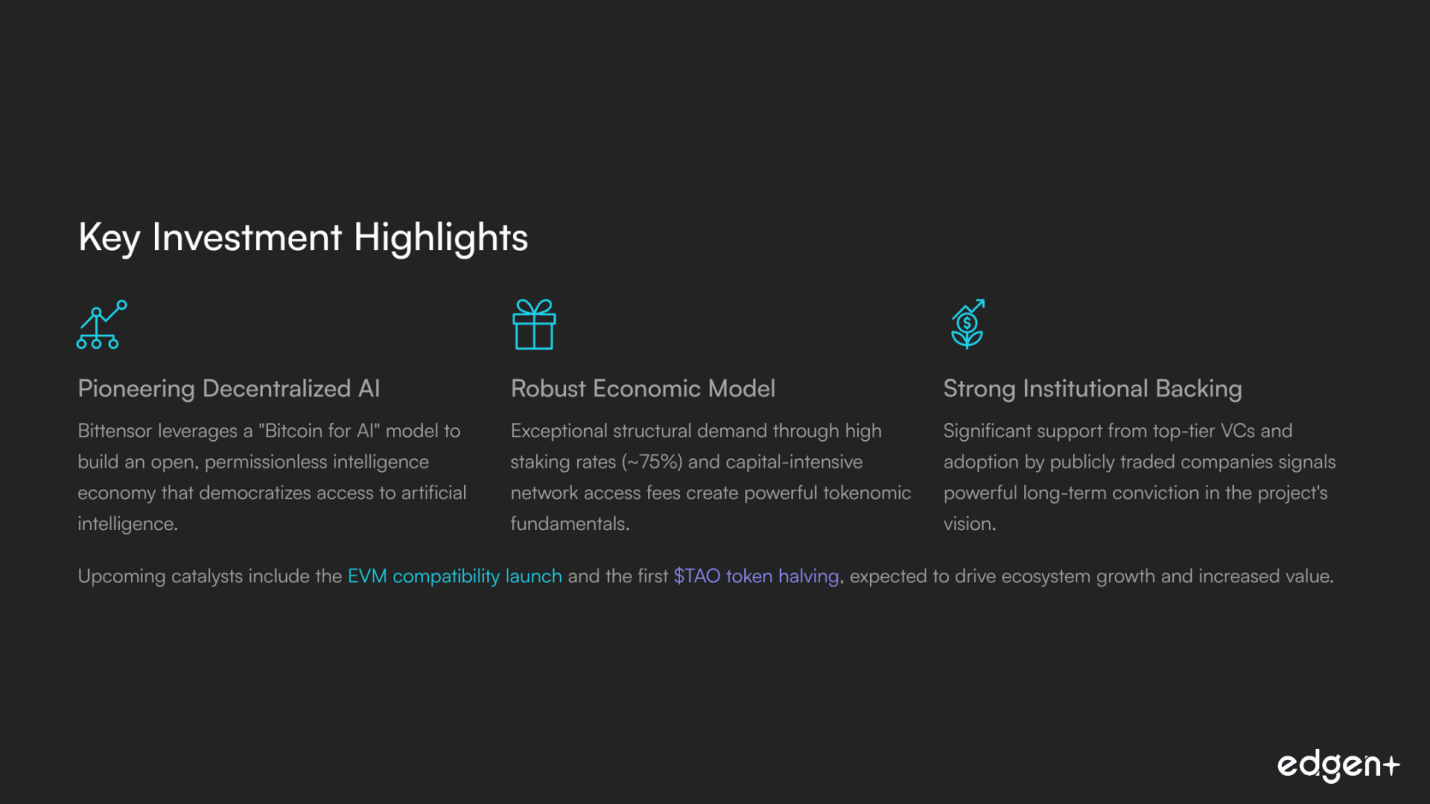

- Bittensor is positioned as a pioneering force in decentralized AI, leveraging a "Bitcoin for AI" model to build an open, permissionless intelligence economy.

- The token's economic model is exceptionally robust, with powerful structural demand created by an exceptionally high staking rate and capital-intensive network access fees.

- The project has secured significant institutional backing from top-tier VCs and has been adopted by publicly traded companies, a powerful signal of long-term conviction.

- Upcoming milestones, including the EVM compatibility launch and the first $TAO token halving, are expected to be major catalysts for ecosystem growth and increased value.

What is Bittensor?

Bittensor's core mission is to create a decentralized, peer-to-peer market for machine intelligence, a vision that powerfully aligns with the most potent themes in the current technology and crypto cycle: Artificial Intelligence (AI) and Decentralized Physical Infrastructure Networks (DePIN). The project directly addresses the risks of centralized AI development by proposing a system where anyone can contribute computational resources or AI models and be rewarded, fostering a more equitable and resilient AI ecosystem. Its tokenomics, which mirror Bitcoin's capped supply and halving schedule, position it not just as a utility token but as a potential monetary primitive for the AI economy, solidifying its multi-faceted and compelling market story.

Part I: Foundational & Strategic Analysis

Strategic Direction & Narrative Trajectory

Bittensor is strategically positioned at the confluence of the powerful decentralized AI and DePIN narratives, leveraging a "Bitcoin for AI" ethos to attract significant market interest and establish itself as a foundational protocol for an open intelligence economy. This visionary positioning ensures the project remains a focal point of discussion and investment as the AI and crypto sectors continue to converge.

Product & Technology Prowess

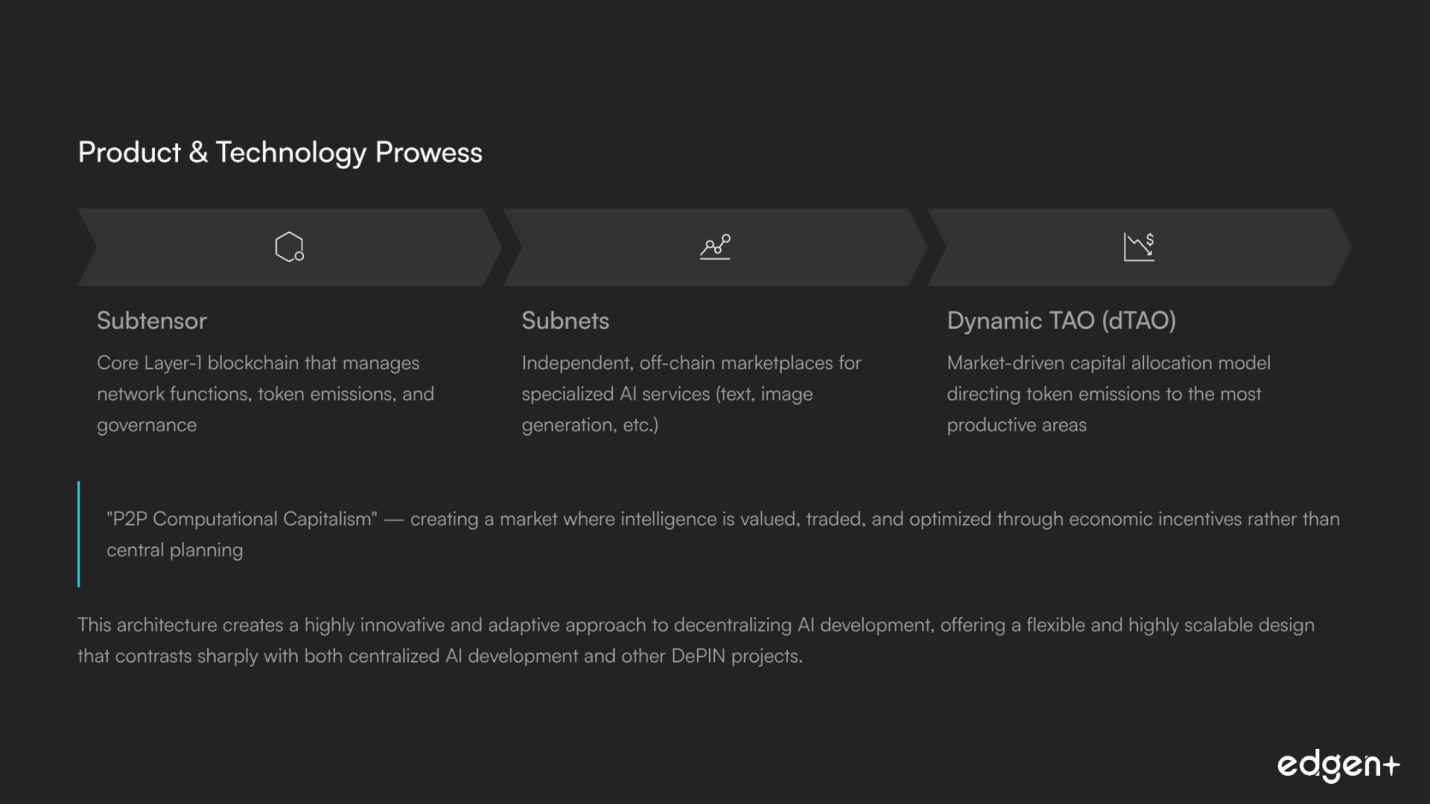

Bittensor's architecture is a highly innovative and adaptive approach to decentralizing AI development. The network is built on a modular two-layer system: the Subtensor, a core Layer-1 blockchain that manages network functions, and numerous Subnets, which are independent, off-chain marketplaces for specialized AI services. The primary innovation is the Dynamic TAO (dTAO) system, which creates a market-driven capital allocation model. This system directs token emissions to the most productive areas of the network, a concept described as "P2P Computational Capitalism." This contrasts sharply with centralized AI development and other DePIN projects, offering a flexible and highly scalable design.

Market Adoption & Developer Activity

The project shows strong early traction in developer and ecosystem adoption, evidenced by a vibrant community and a high velocity of technical development. Data from Stack.money identifies 234 unique developers contributing to the project, with a qualitative review of GitHub showing continuous, professional software development rather than sporadic bursts. This healthy developer ecosystem is complemented by significant on-chain activity, with over 270,000 unique wallets and the rapid growth of active subnets to 125 as of June 2025. The high cost to register a new subnet serves as a financial testament to the perceived value of participating in the ecosystem.

Team & Backers

The founding team's blend of elite software engineering experience from Google and deep academic expertise in computer science and machine learning provides a strong foundation of execution capability. This technical prowess is validated by the project's consistent progress to date. This project is strongly supported by high-conviction crypto-native VCs like Polychain Capital and Digital Currency Group (DCG). It is also pioneering a new model of institutional adoption via direct treasury acquisitions by publicly traded companies like TAO Synergies Inc. and Oblong Inc., lending it significant financial and narrative credibility.

Brand & Ecosystem Longevity

Bittensor has successfully created a powerful brand identity as the "Bitcoin of AI," which has resonated with a broad spectrum of investors and developers. Its strong narrative alignment—spanning AI democratization, DePIN, AI agents, and sound money principles—provides a robust and durable market story. This strong brand, combined with a committed community and an innovative economic model, positions the project for remarkable long-term longevity within the evolving landscape of decentralized technologies.

Part II: On-Chain & Market Depth Analysis

Sustainable Tokenomics & Value Accrual

The TAO token's economic model is robust and well-designed, creating powerful structural demand through an exceptionally high staking rate and significant, capital-intensive barriers to network participation. This demand-side strength provides a formidable counterbalance to the high pre-halving inflation rate. The innovative dTAO mechanism creates a compelling value accrual flywheel where subnet success translates into increased TAO demand and staking, positioning the token as the ecosystem's reserve asset and indispensable key for participation.

Token Holder Distribution & On-Chain Metrics

On-chain data paints a picture of a token with a highly committed holder base, evidenced by a ~75% staking rate of the circulating supply. This suggests that a vast majority of holders are engaged in long-term yield generation and network participation, effectively constraining the liquid, tradable supply. This commitment is a powerful signal of network health and a key driver of the token's stability.

Awareness & Mindshare Analysis

Bittensor exhibits strong and sustained market momentum, supported by a large and growing on-chain holder base, consistently high developer activity, and a resilient community that has transitioned from initial hype to engaged, long-term interest. The project maintains a high level of underlying social engagement, with Rootdata reporting a strong "X Heat" score of 13,148 and Coinpedia noting periods of intense social discussion with up to 3 million interactions. This demonstrates that Bittensor is a major focal point of discussion within the crypto space.

Part III: Forward-Looking Analysis (Catalysts & Risks)

Near-Term Outlook (<1 Month)

- Ongoing Institutional Accumulation: Publicly disclosed acquisitions by entities like TAO Synergies and Oblong Inc. provide a significant and sustained source of demand, creating a strong price floor and signaling conviction to the broader market.

- Daily Token Emissions: The ongoing daily release of tokens is a core component of the network's incentive mechanism, directly funding rewards and ensuring network operation. This managed supply release must be absorbed by new demand.

- Derivatives Market Sentiment: The derivatives market provides a near-term view of market sentiment, with metrics like Open Interest and Funding Rates offering a dynamic, albeit volatile, picture of speculative interest and leverage.

Mid-Term Outlook (1-3 Months)

- EVM Compatibility Launch & Ecosystem Expansion: The introduction of EVM compatibility is a significant technical unlock that dramatically lowers the barrier to entry for the world's largest smart contract developer community. This could lead to a substantial increase in on-chain activity and demand for TAO as a gas and utility token.

- Subnet Scalability & Interoperability Upgrades: These backend upgrades are critical for long-term value, as they improve performance and allow for more complex, composable AI services, making the network more attractive for high-value commercial applications.

- Competitive Landscape: The project operates in a competitive and evolving landscape. The successful execution of roadmaps by competitors could create a narrative and capital competitor, requiring Bittensor to continue its technical leadership to maintain its market position.

Long-Term Outlook (6+ Months)

- First TAO Halving: This is the single most significant, pre-scheduled catalyst for TAO. The reduction of daily emissions in December 2025 will create a substantial supply shock, powerfully reinforcing the "digital scarcity" and "AI Bitcoin" narratives and potentially leading to significant price appreciation.

- Wrapped Staked Alpha Tokens: Enabling staked alpha tokens to be wrapped and traded on other chains would unlock immense liquidity and composability, turning every subnet into its own tradable, yield-bearing asset accessible to the entire DeFi ecosystem.

- AI Sector Narrative Maturity: As the broader AI sector matures, it is essential for projects to demonstrate their fundamental value beyond pure narrative. Bittensor's long-term success is contingent on its ability to prove that its decentralized approach can capture market share from centralized incumbents and its economic model is resilient.

Part IV: Valuation & Competitive Position

Valuation Scenarios

Bittensor's valuation potential is highly promising, spanning a wide range based on both project execution and broader market conditions.

Scenario | Conditions | Justification & Narrative | Target FDV Range |

Bull Case | Strong Execution, Favorable Market | Flawless execution meets strong bull market & narrative. | ≈ US$28.0 B – $42.0 B |

Base Case | Strong Execution, Unfavorable Market | Strong execution and halving create a demand floor. | ≈ US$5.6 B – $10.5 B |

Bear Case | Weak Execution, Favorable Market | Project underperforms despite a strong market. | ≈ US$3.5 B – $7.0 B |

Competitive Landscape

Bittensor occupies a unique position as a meta-protocol for AI services, which differentiates it from more specialized competitors focused on single services like GPU rendering or data indexing. The project’s key differentiators are its "Proof-of-Intelligence" and the Dynamic TAO economic engine, which aim to orchestrate and value the intelligence produced by compute, rather than just providing the raw resources. This positions the project favorably against its peers, with its Base Case FDV projecting a significant value capture within the sector.

Project Name | Primary Focus | Current FDV | Bittensor (Base Case) |

The Graph (GRT) | Decentralized Data Indexing | $0.97 B | $5.6 B - $10.5 B |

Arweave (AR) | Decentralized Storage | $0.44 B | $5.6 B - $10.5 B |

Render (RNDR) | Decentralized GPU Rendering | $1.92 B | $5.6 B - $10.5 B |

NEAR Protocol (NEAR) | AI-focused Layer-1 | $3.18 B | $5.6 B - $10.5 B |

Final Thesis

Bittensor is a high-conviction investment case as a visionary project with a strong foundation and a clear path toward becoming the foundational protocol for a decentralized AI economy. Its robust tokenomic model, reinforced by an exceptionally high staking rate and institutional support, provides a formidable defense against its short-term inflationary pressures. The project is well-positioned for significant long-term growth, with the upcoming 2025 halving serving as a major catalyst. The team's ability to execute on its ambitious roadmap and translate its innovative economic model into a thriving ecosystem of real-world utility remains the ultimate determinant of its long-term success.

Your money person, finally.

Try Ed free. No credit card. No commitment.