Irys Path to a Programmable Future: A New Data Economy

Executive Summary: This report provides a comprehensive analysis of the Irys project, a foundational Layer-1 protocol poised to redefine the intersection of on-chain data and computation. The analysis emphasizes the project's remarkable foundational strength, compelling vision, and significant market opportunities.

TL;DR

- Irys is built on the exceptional, proven execution of a team that has already achieved dominance in the decentralized data sector.

- The project's vision of creating a "programmable datachain" is a promising solution to the fragmentation of Web3 data, positioning Irys to become a premier infrastructure provider for the AI and DePIN sectors.

- Irys has generated significant pre-launch momentum and technical traction, with testnet activity proving the network’s high-throughput capabilities.

- Backed by a top-tier syndicate of infrastructure-focused investors, the project is well-positioned for a successful Token Generation Event (TGE) and mainnet launch, with a high potential for a robust valuation.

What is Irys?

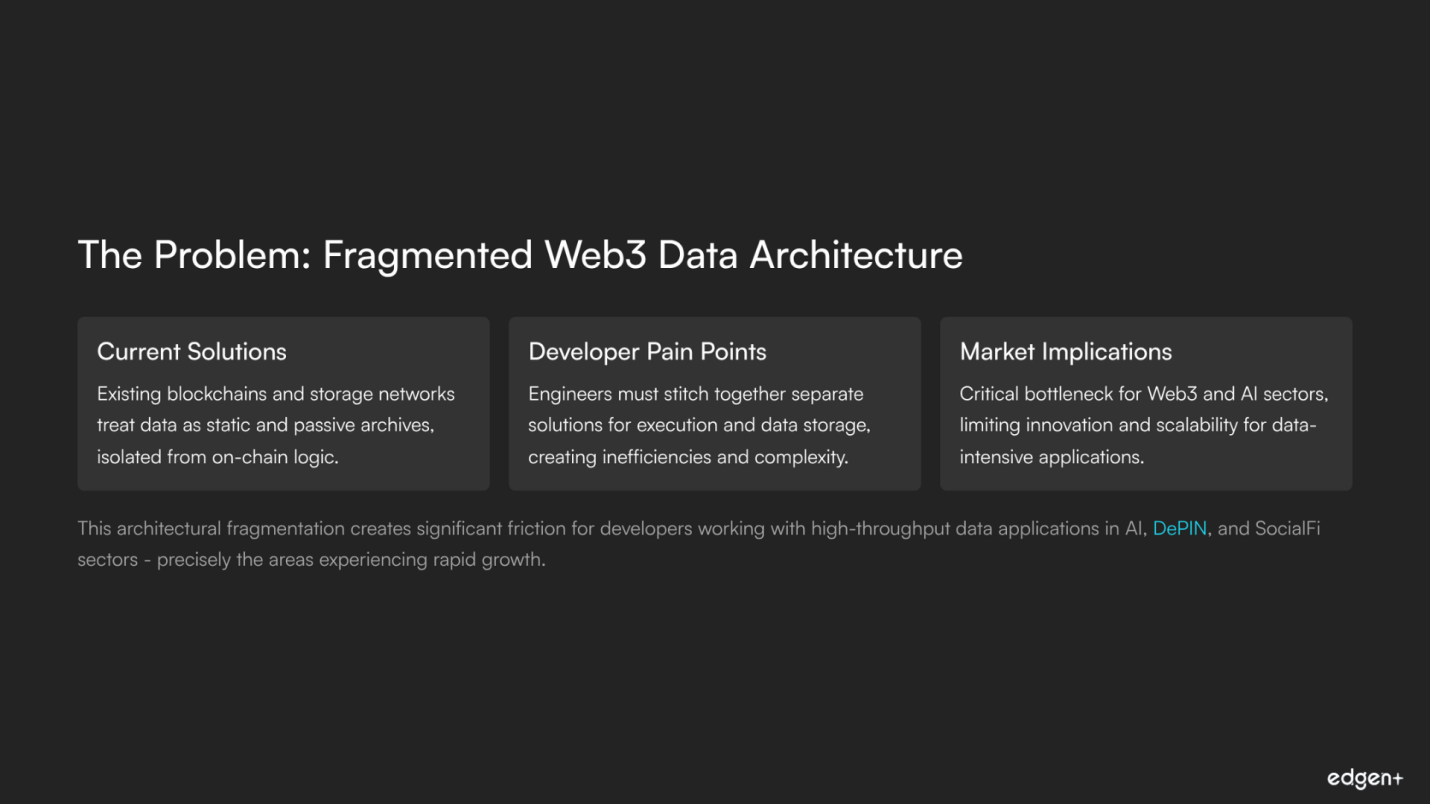

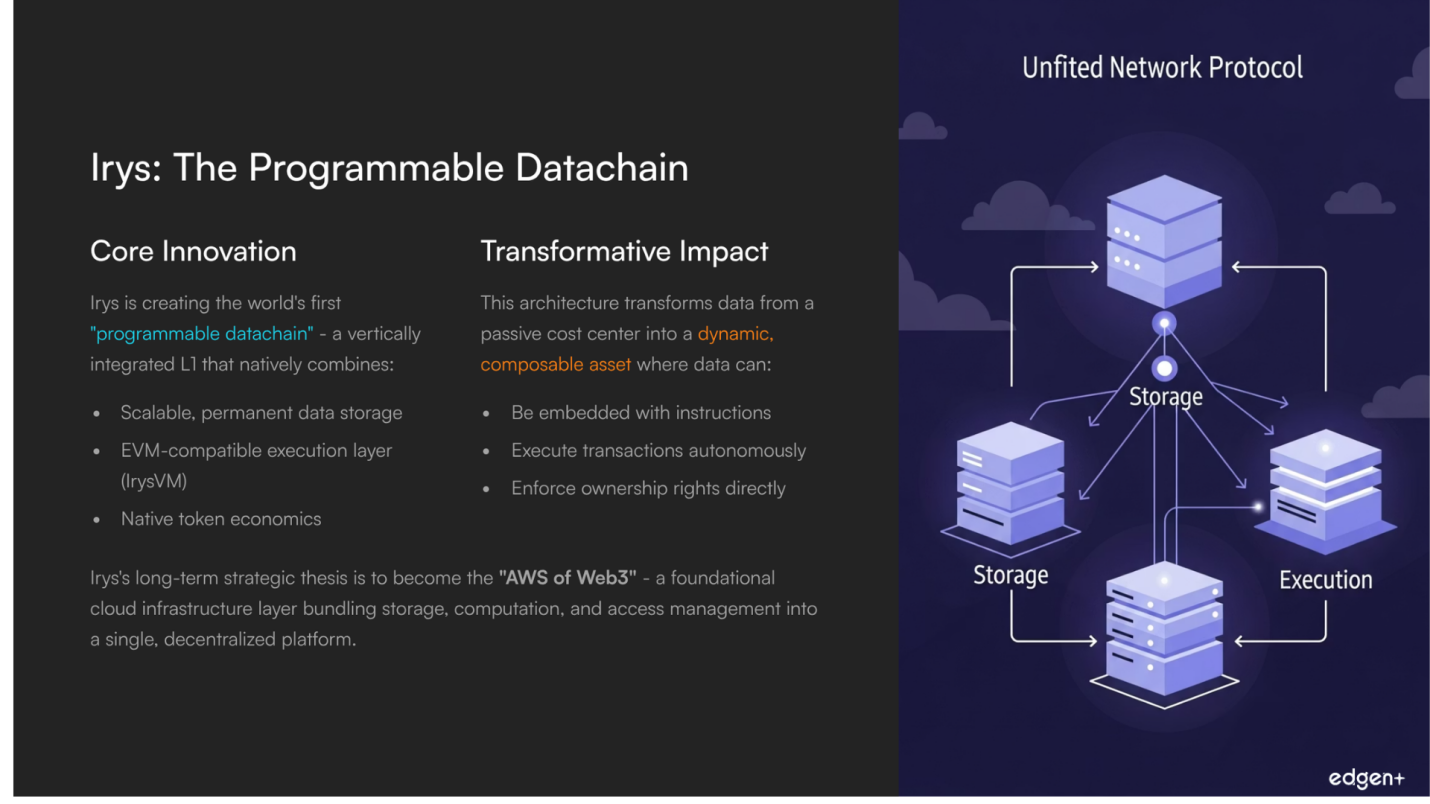

Irys is a foundational Layer-1 protocol designed to solve a critical and growing bottleneck in the Web3 and AI sectors: the architectural fragmentation between on-chain data storage and data computation. The project’s core insight is that existing solutions—whether they are general-purpose blockchains or first-generation decentralized storage networks—treat data as a static, passive archive, isolated from on-chain logic. Irys's mission is to change this by creating the world's first "programmable datachain," a vertically integrated L1 that natively combines scalable, permanent data storage with an EVM-compatible execution layer, the IrysVM.

This unique architecture is designed to transform data from a passive cost center into a dynamic, composable, and monetizable on-chain asset. By providing a unified solution where data can be embedded with instructions, execute transactions, and enforce ownership rights directly on the same network, Irys aims to attract developers in high-throughput sectors like AI, decentralized physical infrastructure networks (DePIN), and SocialFi. The project's long-term strategic thesis is to become the "AWS of Web3," a foundational cloud infrastructure layer that bundles storage, computation, and access management into a single, decentralized, and economically efficient platform.

Part I: Foundational & Strategic Analysis

A Strong and Resilient Foundation

Irys presents a compelling profile with remarkable foundational strength, driven by a credible team, a clear vision, and the backing of sophisticated investors. The project's core hypothesis—that a vertically integrated “programmable datachain” will outperform modular solutions for data-intensive applications—is both ambitious and credible.

Irys's Vision and Investor Alignment

Irys’s core strategic thesis is to solve the architectural fragmentation faced by developers who must currently stitch together separate solutions for execution and data storage. By creating a unified, high-performance datachain, Irys proposes a solution where data can be dynamic and active. This vision is powerfully validated by its backers, which include leading crypto-native VCs like Coinfund, Lemniscap, Framework Ventures, and Hypersphere Ventures. These investors, with a proven track record of supporting foundational infrastructure projects, signal strong conviction that a vertically integrated, data-centric L1 represents a significant and compelling opportunity.

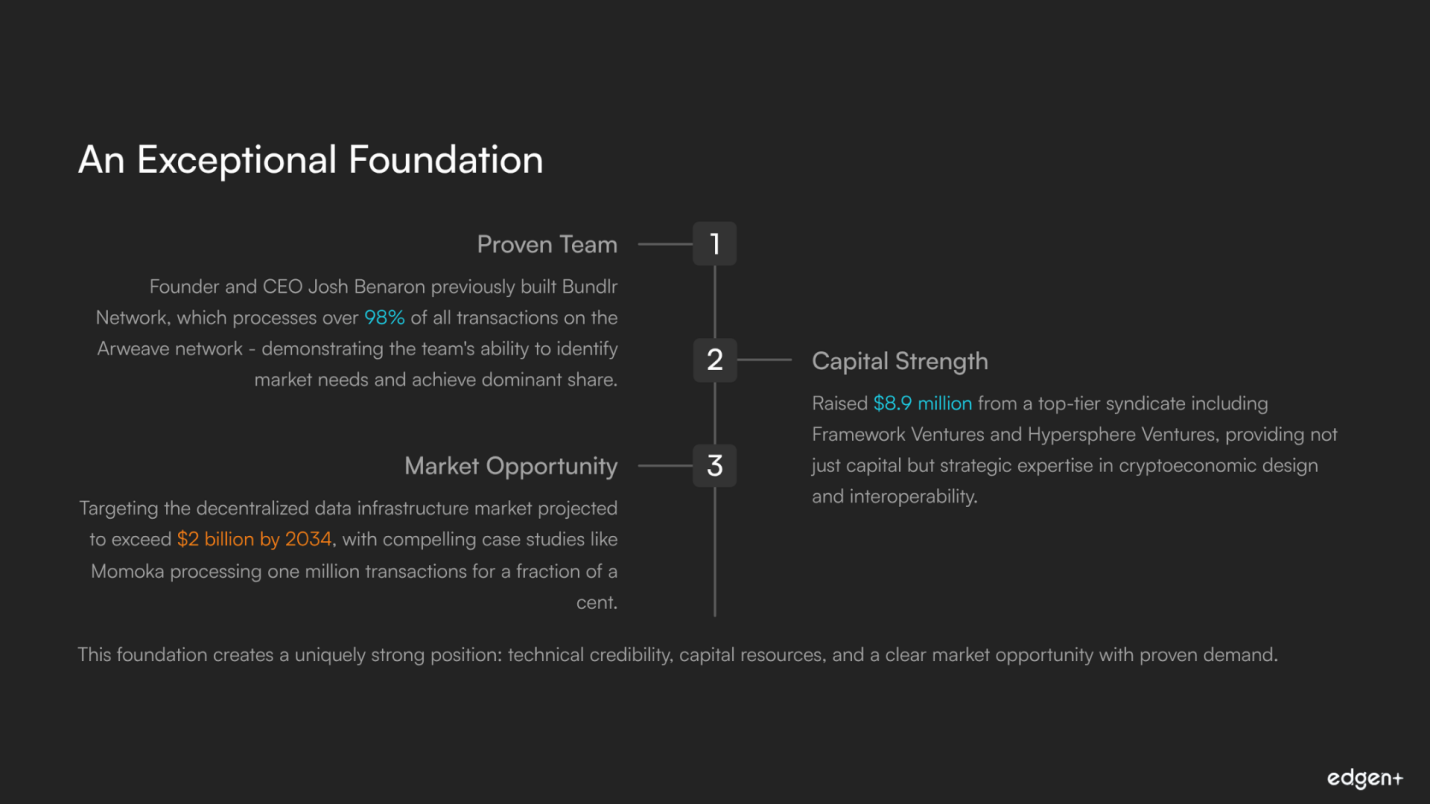

An Exceptional Team with a Proven Track Record

The execution credibility of the Irys team is a standout strength. Founder and CEO Josh Benaron previously built Bundlr Network, which went on to process over 98% of all transactions on the Arweave network. This history provides tangible proof of the team’s ability to identify a critical market need, build a robust solution, and achieve dominant market share. The team's composition, which includes specialists in AI and ecosystem development, suggests a group built not just for technical execution but for strategic growth in its target verticals.

Capital Strength and Strategic Backers

The project is supported by a top-tier syndicate of crypto-native venture capital firms. Having raised a total of $18.9 million, Irys is well-capitalized for an early-stage project. The quality of its lead investors, particularly Coinfund, Framework Ventures and Hypersphere Ventures, provides powerful strategic validation and network effects that extend beyond mere financial backing. These firms bring deep expertise in cryptoeconomic design and interoperability, which is highly relevant to Irys's long-term goals.

The Problem-Solution Fit for a Growing Market

Irys is targeting the rapidly expanding decentralized data infrastructure market. With projections indicating this market will exceed $2 billion by 2034, Irys’s Serviceable Addressable Market (SAM) is substantial. The project’s value proposition is centered on delivering superior performance, new capabilities via the IrysVM, and significant cost savings. The team's prior success with Bundlr and case studies like Momoka, which processed one million transactions for a fraction of a cent, provide compelling evidence of the economic efficiencies it can enable.

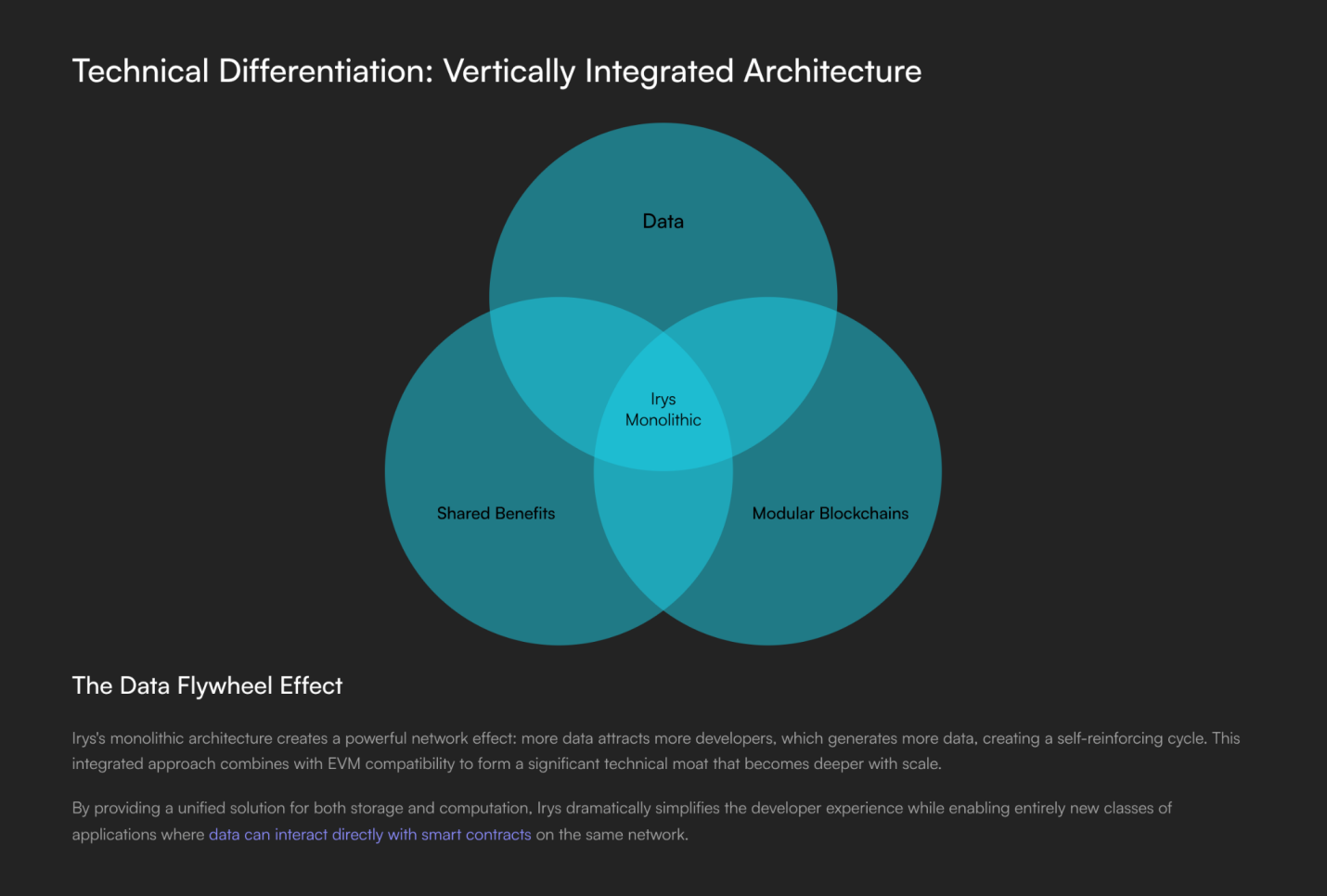

The Distinctive Competitive Edge

Irys's primary technical differentiator is its monolithic, vertically integrated architecture, which stands in stark contrast to the modular approach of competitors. By fusing a storage layer with an EVM-compatible execution layer, Irys aims to create a "data flywheel" where more data attracts more developers, creating a compounding network effect. This integrated approach, combined with EVM compatibility, forms the basis of its potential long-term moat.

Part II: Pre-Launch Ecosystem & Go-to-Market Analysis

A Powerful and Dynamic Pre-Launch Strategy

Irys has executed a potent pre-launch strategy that has generated significant traction and momentum. This approach showcases the team's ability to engage with and build a vibrant community, laying the groundwork for a successful launch.

Strong Narrative and Community Momentum

The project has successfully aligned its narrative with some of the market’s most compelling themes, including AI, DePIN, and decentralized infrastructure. This is reflected in its consistent ranking within the top 10 of the Kaito project leaderboard, a key indicator of community attention and mindshare. Irys's ability to drive community growth and social engagement demonstrates a strong go-to-market capability for initial awareness and a high level of market anticipation.

Remarkable On-Chain Traction

Irys has proven its technical capacity through a well-executed testnet incentive program. The network has processed over 200 million data transactions and accumulated over 465 GB of data, with a reported 1.5 million active addresses. These metrics validate the network’s technical architecture and its ability to handle high throughput, serving as a powerful demonstration of the team's ability to execute a large-scale user acquisition campaign.

Strategic Partnerships and Ecosystem Readiness

Irys has secured a notable portfolio of pre-launch partnerships that signal both technical validation and a coherent go-to-market strategy. Key integrations with OKX Wallet, Berachain, and various AI-focused projects (FXN AI, SCAI) provide critical distribution channels and reinforce the project's positioning. These collaborations represent other development teams actively building on or integrating with Irys’s infrastructure, a powerful endorsement of the technology.

Part III: Forward-Looking Analysis (Catalysts & Risks)

Near-Term Outlook: A Major TGE Catalyst

Irys is poised for a significant milestone: its Mainnet Launch and Token Generation Event (TGE). This is the primary near-term catalyst that will transition the project from a testnet to a live, production-grade protocol, unlocking its initial public market valuation. A successful launch, especially with a top-tier exchange listing, would be a powerful endorsement and likely lead to a positive re-rating of the project's valuation.

Long-Term Outlook: The Promise of Developer Adoption

The most significant long-term catalyst for Irys is the demonstrable adoption of its IrysVM by developers. Successful adoption of its "programmable data" features would validate the project’s core thesis and establish it as a category creator. A growing number of applications building on Irys would drive transaction volume, data uploads, and token demand, creating a sustainable economic flywheel and cementing its position as a long-term leader in the space.

Part IV: Valuation Scenario Analysis

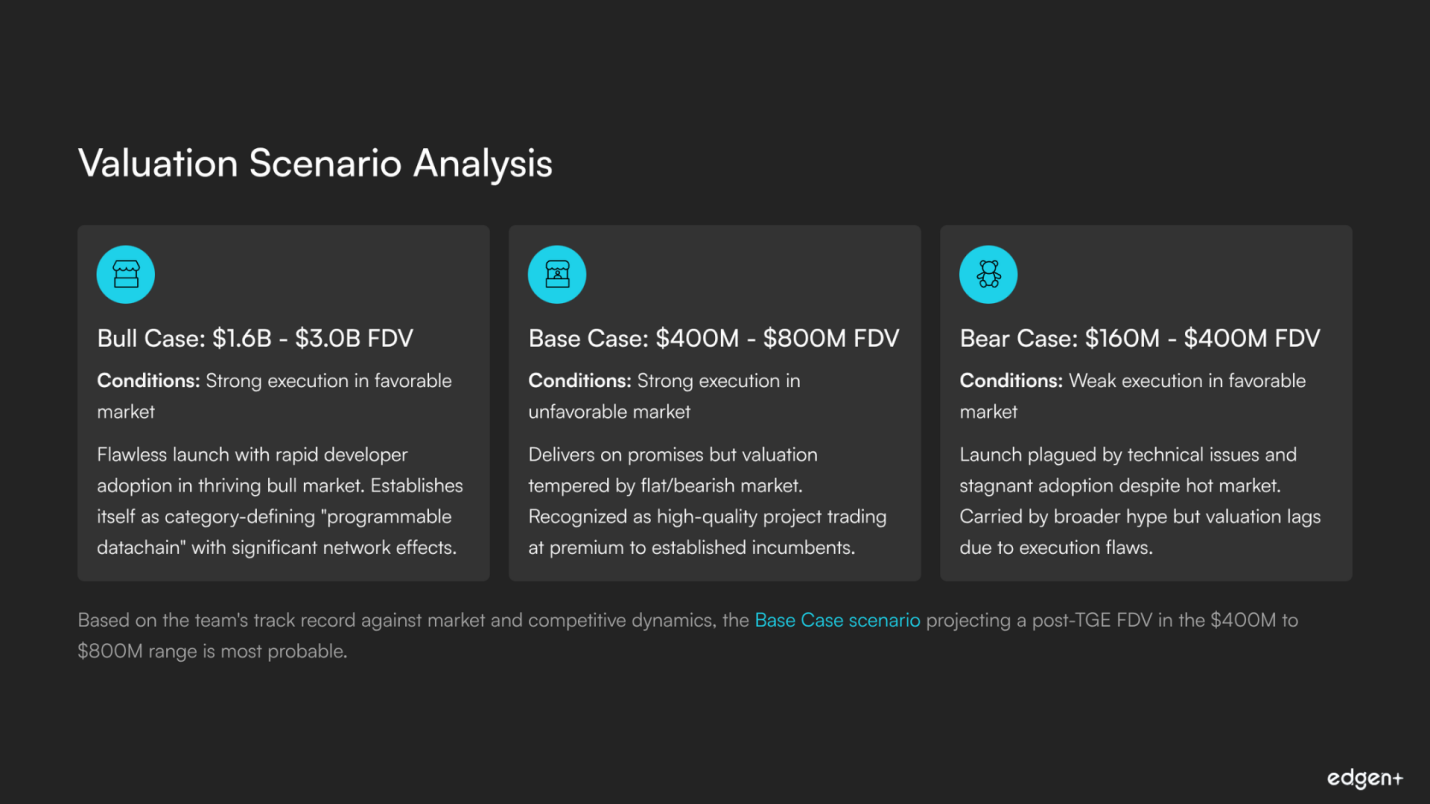

TGE Forecast Scenarios

This analysis provides a structured valuation framework to project Irys's potential Fully Diluted Valuation (FDV) 6-12 months post-TGE. The scenarios are based on a combination of internal project execution and external market conditions.

Scenario | Conditions | Justification & Narrative | Projected Outcome (Post-TGE FDV) |

Bull Case | Strong Execution, Favorable Market | Irys executes a flawless launch and achieves rapid developer adoption in a thriving bull market. The project successfully establishes itself as a category-defining "programmable datachain." | $1.6B - $3.0B |

Base Case | Strong Execution, Unfavorable Market | Irys delivers on its promises, but its valuation is tempered by a flat or bearish broader crypto market. It is recognized as a high-quality project, trading at a valuation comparable to or slightly above established incumbents. | $400M - $800M |

Bear Case | Weak Execution, Favorable Market | Despite a hot market, the launch is plagued by technical issues and stagnant adoption. The project is carried by market hype, but its valuation lags significantly due to execution flaws. | $160M - $400M |

Competitor Landscape: TGE Token Comparison (Base Case)

This table compares Irys's projected Base Case FDV with the current Fully Diluted Valuations of key established competitors in the decentralized data and modular blockchain space, providing context for its potential market positioning.

Project (TGE Token) | Sector | Current/Projected FDV (Billions of USD) | Notes |

Programmable Datachain (L1) | $0.4B - $0.8B | Irys's projected Base Case post-TGE FDV, emphasizing strong execution despite potentially challenging market conditions. | |

Permanent Decentralized Storage | ~$0.45B - $0.46B | An established incumbent focused on permanent data storage, from which Irys originated. | |

Data Availability Layer (Modular) | ~$1.9B - $2.8B | A leading modular blockchain focused on data availability, vital for rollups and scalable dApps. | |

Decentralized Storage Network | ~$4.7B - $4.9B | The largest decentralized storage network by capacity, offering a marketplace for storage providers and clients. |

Final Thesis

Irys presents a compelling and high-potential investment case, anchored by a proven team and a syndicate of elite VCs. The project’s vision for a “programmable datachain” is technically sound and targets a substantial market need. The valuation outcome is overwhelmingly dependent on the team's ability to execute a smooth launch and achieve genuine, organic developer adoption of its IrysVM. Based on the strength of the team against market and competitive headwinds, the Base Case scenario, projecting a post-TGE FDV in the $400M to $800M range, is the most probable outcome.

Your money person, finally.

Try Edgen free. No credit card. No commitment.