TL;DR

- Monad boasts exceptional foundational strength, backed by a world-class team with a unique background in high-frequency trading (HFT) and a substantial $244 million in funding from premier venture capital firms.

- The project’s pre-launch momentum is remarkable, with a massive and engaged community, a powerful narrative, and a robust lineup of strategic ecosystem partners.

- Monad presents a compelling and promising solution to the long-standing scalability constraints of the EVM, potentially unlocking a new generation of high-throughput decentralized applications.

- While the path forward presents inherent risks, particularly related to a lack of public clarity on its tokenomics, the project's core strengths position it for a very promising future.

Foundational & Strategic Analysis

Monad’s Vision & Investor Alignment

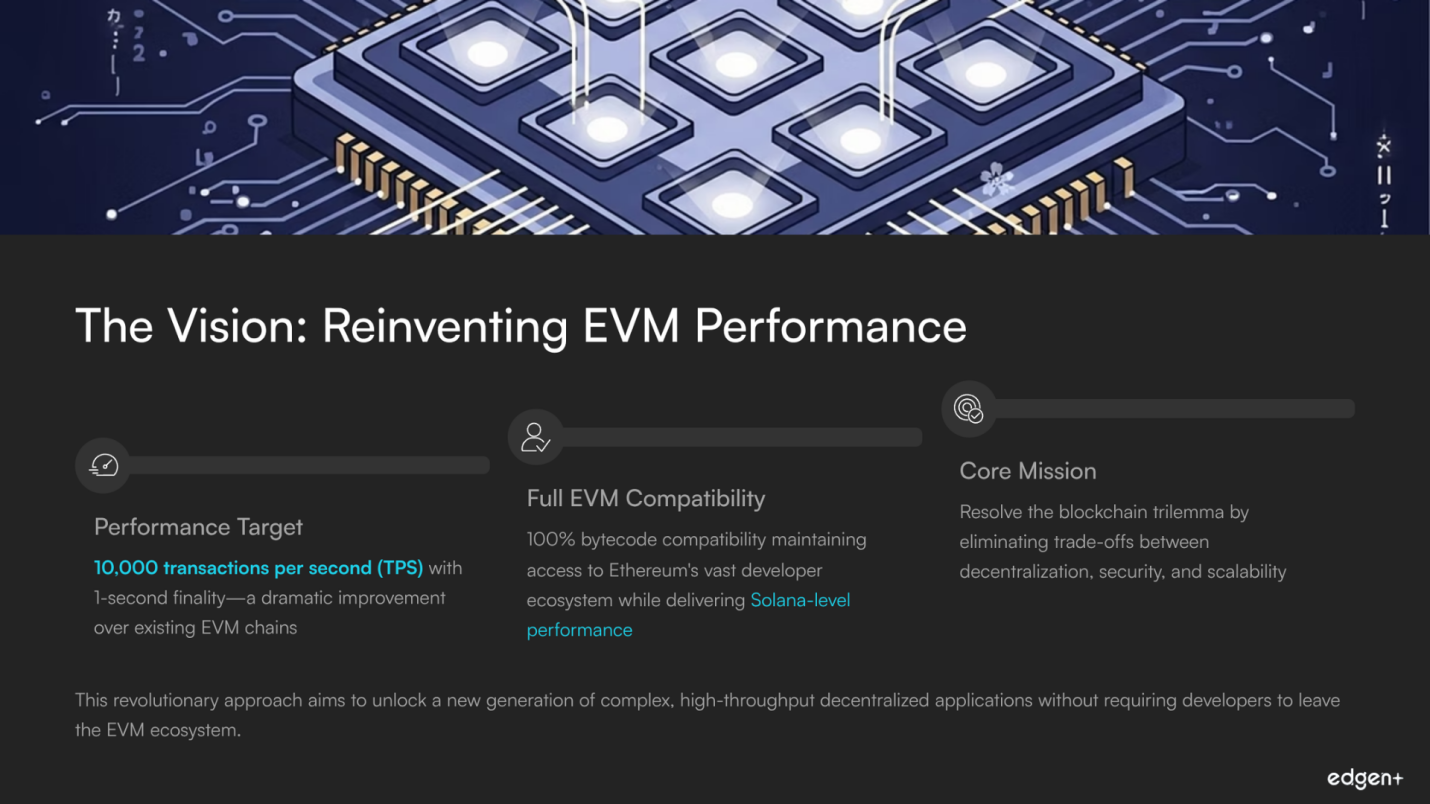

Monad's strategic vision is to fundamentally re-architect the Ethereum Virtual Machine (EVM) execution layer to resolve the persistent trade-offs between decentralization, security, and scalability. The project’s core mission is to build a Layer 1 (L1) blockchain that delivers massively parallel performance without sacrificing EVM compatibility. This approach aims to unlock the potential for a new generation of complex, high-throughput decentralized applications.

This vision is supported by a concrete performance target of 10,000 transactions per second (TPS), representing a significant improvement over existing EVM chains. By delivering this level of performance, Monad aims to eliminate the compromise developers currently face between the vast network effects of the EVM ecosystem and the superior performance of non-EVM chains like Solana. This thesis directly challenges the prevailing market structure.

This ambitious vision is strongly validated by Monad’s backers, led by the premier crypto-native venture firm, Paradigm. Their commitment of $225 million in a funding round that valued the pre-product company at $3 billion signals a high-conviction belief in the team's technical credibility and the market-defining potential of a truly performant, parallelized EVM.

Exceptional Team and Execution Prowess

The Monad team’s execution credibility is remarkably high, anchored by a unique combination of elite low-latency systems engineering and seasoned product leadership. Co-founder & CEO Keone Hon and Co-founder & CTO James Hunsaker both have a background at Jump Trading, a globally recognized leader in high-frequency trading (HFT). This experience is directly applicable to the core challenge of blockchain performance, providing the team with a significant and defensible differentiator. Their technical prowess is complemented by Co-founder & COO Eunice Giarta, who brings extensive product management experience to ensure the project’s profound technical depth is guided by a pragmatic product vision.

The project's organizational growth demonstrates a strategic and maturing approach, with recent hiring focused on crucial go-to-market and operational roles. This expansion signals a clear intent to build the business and community infrastructure necessary for a successful launch and long-term growth. The team has shown proactive, forward-looking decision-making by addressing potential skill gaps and building a well-rounded organization capable of competing on multiple fronts.

Premier Backers & Capital Strength

Monad is supported by a formidable coalition of top-tier, crypto-native venture capital firms and influential angel investors. The project has raised a total of $244 million, headlined by the $225 million Series A round led by Paradigm. The participation of other leading funds like Dragonfly Capital, Electric Capital, and Greenoaks Capital further solidifies its institutional endorsement. The implication of this backing extends beyond capital; it serves as a powerful market signal that validates the project's ambitious technical vision and the team's perceived ability to execute. This "smart money" endorsement provides a significant competitive advantage in attracting talent, securing partnerships, and building initial ecosystem momentum.

The project's capitalization is exceptionally robust for a pre-launch entity, affording it a multi-year operational runway to navigate the complexities of mainnet launch, ecosystem development, and potential market downturns. The valuation of $3 billion achieved during the Series A round underscores the high expectations of its investors and sets a significant benchmark for future performance.

Significant Market Opportunity

Monad is targeting a vast and clearly defined market opportunity: the entire ecosystem of decentralized applications bottlenecked by the performance limitations of the Ethereum Virtual Machine. The project demonstrates a strong and compelling problem-solution fit by directly addressing the primary pain points of its target buyer personas: developers of sophisticated, high-throughput applications. For DeFi protocol developers, particularly those building on-chain order books or high-frequency strategies, the low latency and 10,000 TPS target of Monad offer a path to an on-chain user experience that can compete with centralized finance. For GameFi studios, Monad’s architecture promises the ability to support complex in-game economies and real-time interactions at scale.

A critical component of Monad's problem-solution fit is its commitment to full EVM bytecode compatibility. This significantly lowers adoption friction and switching costs for its target market, allowing Monad to leverage Ethereum's immense network effects—its established developer community, extensive documentation, and battle-tested infrastructure—while offering a vastly superior performance profile. This combination of radical performance improvement with conservative, developer-friendly compatibility is a powerful driver for adoption.

Competitive Landscape & Differentiators

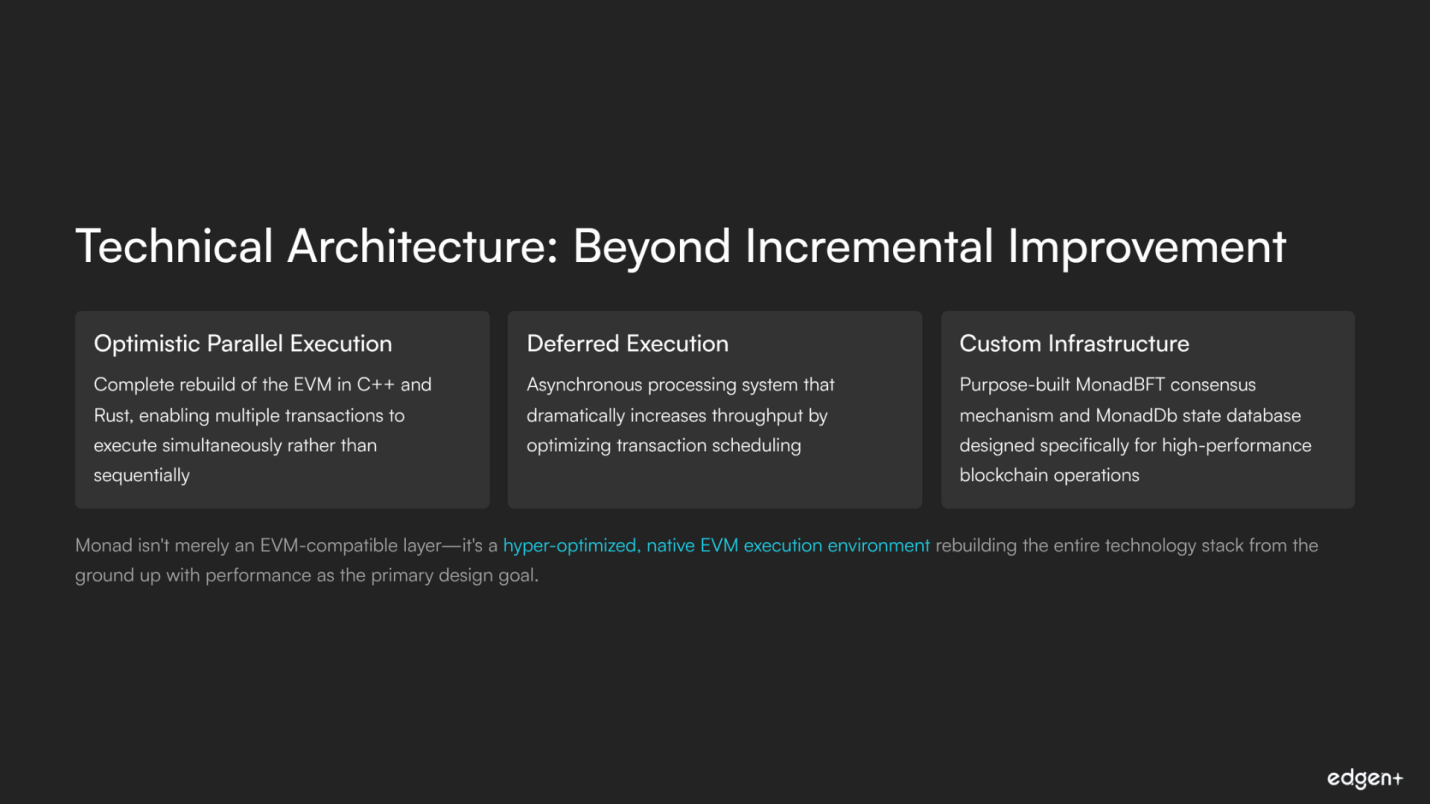

Monad enters a highly competitive landscape but is armed with a potent and defensible set of differentiators rooted in its unique technical architecture and strategic market positioning. The project's core differentiator against all competitors is its unique value proposition: delivering Solana-level performance while maintaining 100% EVM bytecode compatibility. This is achieved by rebuilding the EVM from the ground up in C++ and Rust, incorporating deep optimizations like optimistic parallel execution, asynchronous processing (Deferred Execution), a custom consensus mechanism (MonadBFT), and a purpose-built state database (MonadDb). The implication of this full-stack overhaul is that Monad is not merely an EVM-compatible layer but a hyper-optimized, native EVM execution environment.

The project’s narrative differentiation is exceptionally sharp and memorable, effectively positioning Monad as the resolution to the primary dilemma facing blockchain developers today. The narrative can be distilled to "the best of both worlds," combining the performance and low fees of alternative L1s with the unparalleled developer ecosystem, liquidity, and network effects of Ethereum. This story is compelling because it directly addresses the high switching costs—both technical and mental—that have prevented a mass developer exodus from Ethereum.

Pre-Launch Ecosystem & Go-to-Market Analysis

Remarkable Community & Narrative Momentum

Monad has successfully cultivated a large-scale, highly active community and a potent pre-launch narrative, positioning it with a level of social momentum typically reserved for established, post-launch networks. The project’s primary X account (@monad_xyz) serves as the focal point of this strategy, having amassed an audience of 1.3 million followers. This figure is substantiated by exceptionally high engagement levels on key announcements. This massive, engaged audience creates a powerful and cost-effective distribution channel for go-to-market initiatives, significantly reducing the friction for both the core protocol and its emerging ecosystem of dApps to acquire their initial user base.

The project’s narrative strength is anchored in a clear and compelling message: delivering the performance of alternative L1s like Solana while maintaining full EVM compatibility. This "best of both worlds" value proposition resonates strongly within the crypto developer and user communities. Strategic community-building, which combines targeted regional expansion with a universally appealing technical narrative, creates a formidable moat of mindshare that is difficult for competitors to replicate.

Promising Pre-Launch Traction

Monad's testnet has generated on-chain metrics of a magnitude that suggests both immense interest and the significant presence of automated or Sybil-related activity. The network has successfully processed a peak of over 22.6 million daily transactions and deployed a vast number of smart contracts, with figures ranging from 110,300 to a staggering 6.8 million. This demonstrates that the underlying infrastructure can handle a high degree of programmatic interaction, a key requirement for attracting sophisticated DeFi and gaming applications. The testnet has effectively served as a large-scale stress test, proving the viability of Monad's parallel execution architecture and giving confidence to the over 100 projects reportedly building within the ecosystem. Therefore, while the on-chain footprint is a noisy indicator of user traction, it is a strong signal of developer traction and technical readiness.

Strategic Partnerships & Go-to-Market Readiness

Monad has executed a highly effective partnership strategy focused on establishing deep, technical integrations with critical Web3 infrastructure, ensuring a mature and developer-friendly ecosystem from day one of its mainnet launch. The project has secured day-one support from a roster of industry-standard providers, which is a strong indicator of go-to-market readiness. This includes oracle services from both Chainlink (Data Feeds, Data Streams, CCIP) and Pyth Network; node and API infrastructure from Alchemy; and interoperability solutions from LayerZero and Wormhole. The native integration of USDC, facilitated by a partnership with Circle, is particularly noteworthy, as it removes a major liquidity and usability friction point for DeFi applications.

Beyond foundational infrastructure, Monad has fostered a burgeoning ecosystem of native and migrating applications, signaling strong early-stage developer conviction in the platform's potential. The emergence of multiple, competing liquid staking protocols prior to mainnet—including Magma, Kintsu, and aPriori—is a particularly strong vote of confidence. Furthermore, partnerships with platforms like GameBuild for gaming infrastructure and the existence of a native launchpad, Monad Pad, indicate a strategic focus on key growth verticals. This proactive ecosystem development, which has reportedly attracted over 80 protocols, provides tangible evidence that Monad's value proposition is resonating with builders and that a diverse set of applications will be available to users at or shortly after launch.

Forward-Looking Analysis (Catalysts & Risks)

The forward-looking outlook for Monad is characterized by a singular, high-impact catalyst—the mainnet launch—set against a backdrop of considerable uncertainty stemming from pervasive information gaps.

Mainnet Launch: The Primary Catalyst

The Mainnet Launch & Token Generation Event (TGE) is expected in Late 2025 (Q4). This event is the primary catalyst to unlock Monad's valuation. A successful launch, particularly if accompanied by a listing on a top-tier exchange, will establish the first public market valuation (FDV) for Monad, crystallizing its position relative to competitors like Solana, Sui, and Aptos.

The launch will transition Monad from a theoretical project to a live network, initiating on-chain activity and testing the performance claims of 10,000 TPS and 1-second finality in a real-world environment. A smooth and performant mainnet launch would powerfully validate the project's core narrative of delivering "Solana performance with Ethereum compatibility," shifting the conversation from potential to demonstrated capability.

Important Technical Milestones

The Testnet 1 Upgrade, confirmed for November 1, 2025, is a positive signal of development momentum and execution capability. A successful upgrade demonstrates the team's ability to manage and improve the network, building confidence in their capacity to handle the more complex mainnet launch. It is a crucial step in the pre-launch hardening process, reinforcing the narrative of active and ongoing development.

Key Areas for Continued Monitoring

Despite its immense potential, Monad faces considerable uncertainty stemming from persistent information gaps, which should be closely monitored:

- Critical Information Gaps: There is an ongoing lack of publicly available, detailed information regarding the project's official roadmap, financial plan, tokenomics, and legal structure. This opacity prevents thorough due diligence and may delay or prevent commitments from sophisticated actors.

- Ambiguous Tokenomics: The complete failure to retrieve any data on token allocations or emissions for the MON token creates significant uncertainty around future sell pressure. This lack of clarity on vesting schedules for the team and investors can suppress initial valuation and deter long-term holders.

- Post-Launch Roadmap Uncertainty: The consistent failure to uncover any official roadmap detailing milestones beyond the initial mainnet launch suggests a lack of long-term strategic communication. Without a clear roadmap for future features, Monad risks being perceived as a "one-trick pony," potentially leading to valuation compression.

- Unresolved Regulatory Status: The failure to identify Monad's corporate structure or legal jurisdiction in any research phase is a notable area for future clarification.

Valuation Scenario Analysis

This analysis synthesizes all preceding findings into a valuation matrix to project Monad's potential Fully Diluted Valuation (FDV) 6-12 months post-TGE. The framework is contingent on two critical, independent variables: the project's internal execution capability and the external state of the broader cryptocurrency market. The last known private valuation of US$3 billion serves as the primary benchmark for these scenarios.

Projected FDV Scenarios

This table outlines the potential FDV ranges for Monad, contingent on its execution and the broader market environment.

Scenario | Conditions | Narrative | FDV Target Range (in billions) |

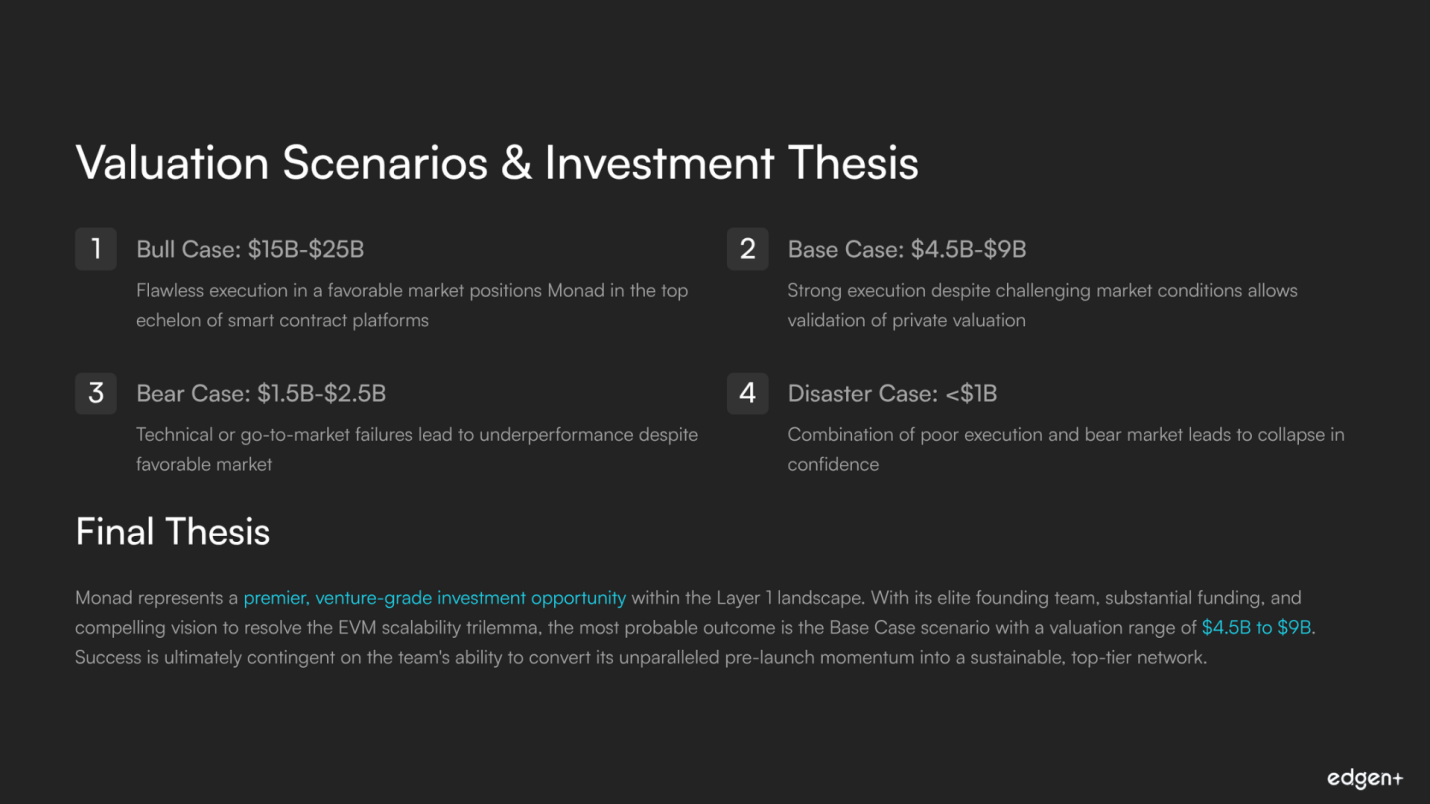

Bull Case | Strong Execution & Favorable Market | Monad’s flawless execution in a risk-on environment positions it as the premier new L1. Its EVM compatibility and demonstrated performance justify a valuation premium, placing it in the top echelon of smart contract platforms. The combination of a world-class team, validated technology, and a bull market creates the conditions for exponential value accrual. | ≈ US$15B - $25B |

Base Case | Strong Execution & Unfavorable Market | Despite a challenging market, Monad's strong execution allows it to stand out as a high-quality, fundamentally sound project. It successfully captures market share and validates its private valuation. Its potential is capped by the broader market downturn, causing it to trade in line with or slightly above established peers like Aptos or Sui. | ≈ US$4.5B - $9B |

Bear Case | Weak Execution & Favorable Market | Monad fails to deliver on its technical promises or its go-to-market strategy, leading to stagnant user growth. Despite a favorable bull market, the project underperforms its peers, failing to justify its high private valuation and trading at a discount. It is perceived as a disappointment, unable to achieve fundamental adoption. | ≈ US$1.5B - $2.5B |

Disaster Case | Weak Execution & Unfavorable Market | The combination of poor execution and a bear market proves catastrophic. A failed launch or critical technical issues lead to a lack of market interest and immense sell pressure. The project's high valuation becomes an anchor, leading to a collapse in confidence and a risk of becoming an irrelevant "ghost chain." | < US$1B |

Final Thesis

Monad represents a premier, venture-grade investment opportunity within the Layer 1 landscape, distinguished by an elite founding team with a unique HFT background, a formidable $244 million in funding, and a compelling vision to resolve the EVM scalability trilemma. This exceptional foundational strength is, however, balanced by important risks, including the immense challenge of executing a flawless mainnet launch into a hyper-competitive market and a need for greater transparency regarding its post-launch roadmap, tokenomics, and legal structure.

Synthesizing these factors, the most probable outcome is the Base Case scenario, where strong execution validates the core technology but a neutral-to-unfavorable market caps its valuation in the $4.5B to $9B range. Ultimately, Monad offers a high-beta return profile where success is entirely contingent on the team's ability to convert its unparalleled pre-launch momentum and technical promise into a sustainable, top-tier network capable of justifying its landmark private valuation.

Your money person, finally.

Try Edgen free. No credit card. No commitment.