An outlook on Somnia’s specialized L1 for metaverse and gaming, covering strategy, partners, token model, catalysts, and valuation. For a simple guide for new users, click here

TL;DR

- Specialized L1 for real-time apps: Architecture (MultiStream Consensus, Accelerated Sequential Execution, IceDB) targets hot-state workloads other chains struggle with.

- Backed to execute: Up to $270M in ecosystem funding via Improbable/MSquared, Google Cloud validator/infrastructure, and a $10M Dream Catalyst to seed games, positioning Somnia to convert narrative into shipped products.

What is Somnia

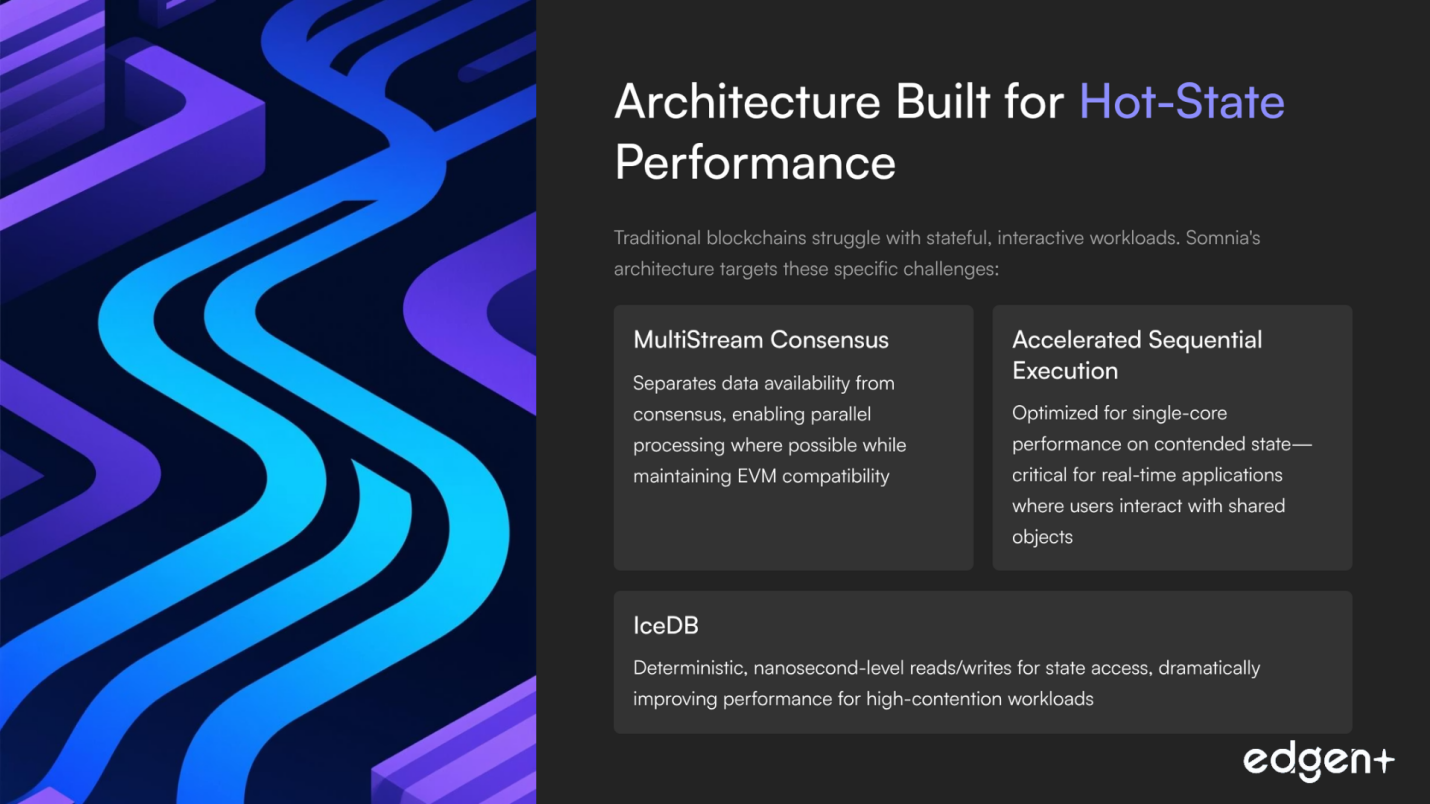

Somnia is an EVM-compatible Layer-1 engineered for metaverse-scale performance: sub-second finality, sub-cent fees, and 1M+ TPS targets. Rather than chasing general DeFi throughput, Somnia is optimized for stateful, interactive workloads—MMOs, social graphs, on-chain economies—using a design that accelerates single-core execution for hot contention while leveraging hardware parallelism. Its MultiStream Consensus separates data availability from consensus, and IceDB aims for deterministic, nanosecond-level reads/writes.

Backed by Improbable/MSquared’s deep experience in virtual worlds, Somnia aligns infrastructure with developer reality: familiar EVM tooling, a low-code builder stack (via partners), and a well-funded accelerator to bring content on day one. With Google Cloud supporting validation and AI/data security services, and studios like Realm (Variance) preparing to build, Somnia’s proposition is clear: a “dream computer” where Web3 experiences feel instant and composable—ready for mainstream users.

I. Foundational & Strategic Analysis

1) Vision & Investor Alignment

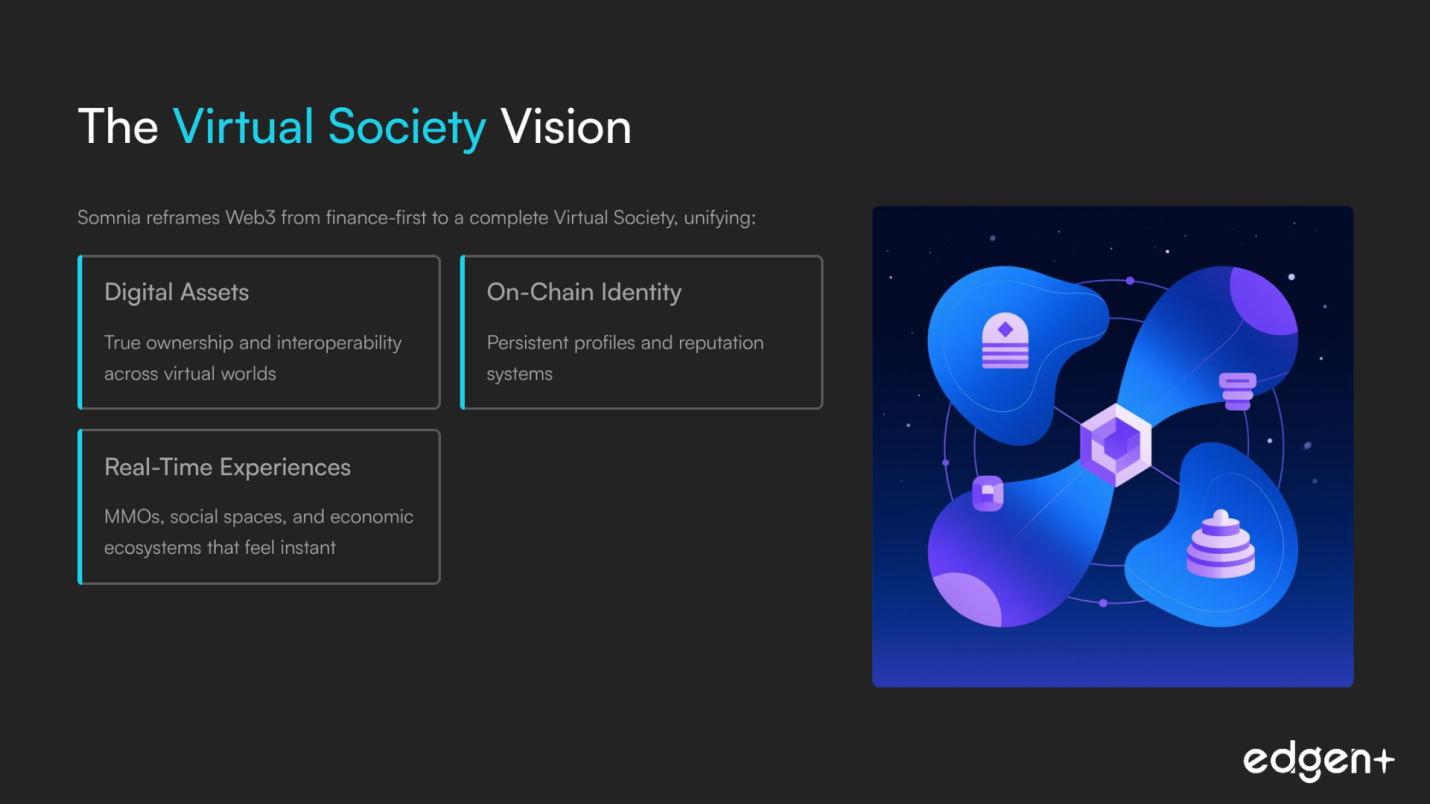

Somnia’s thesis is focused: become the specialized L1 for metaverse/social/gaming, where performance, latency, and cost decide winners. The strategy reframes Web3 from finance-first to Virtual Society, unifying assets, identity, and experiences. Partnerships (e.g., Yuga Labs alignment) and a $10M accelerator signal long-term commitment to content and developer success.

2) Team & Execution Prowess

Founder Paul Thomas (Improbable) brings rare distributed-systems depth; Michelle Kang adds L1/L2 growth expertise. The blend of infra rigor and GTM know-how supports complex protocol delivery and ecosystem onboarding, very promising for a new L1.

3) Capital & Endorsements

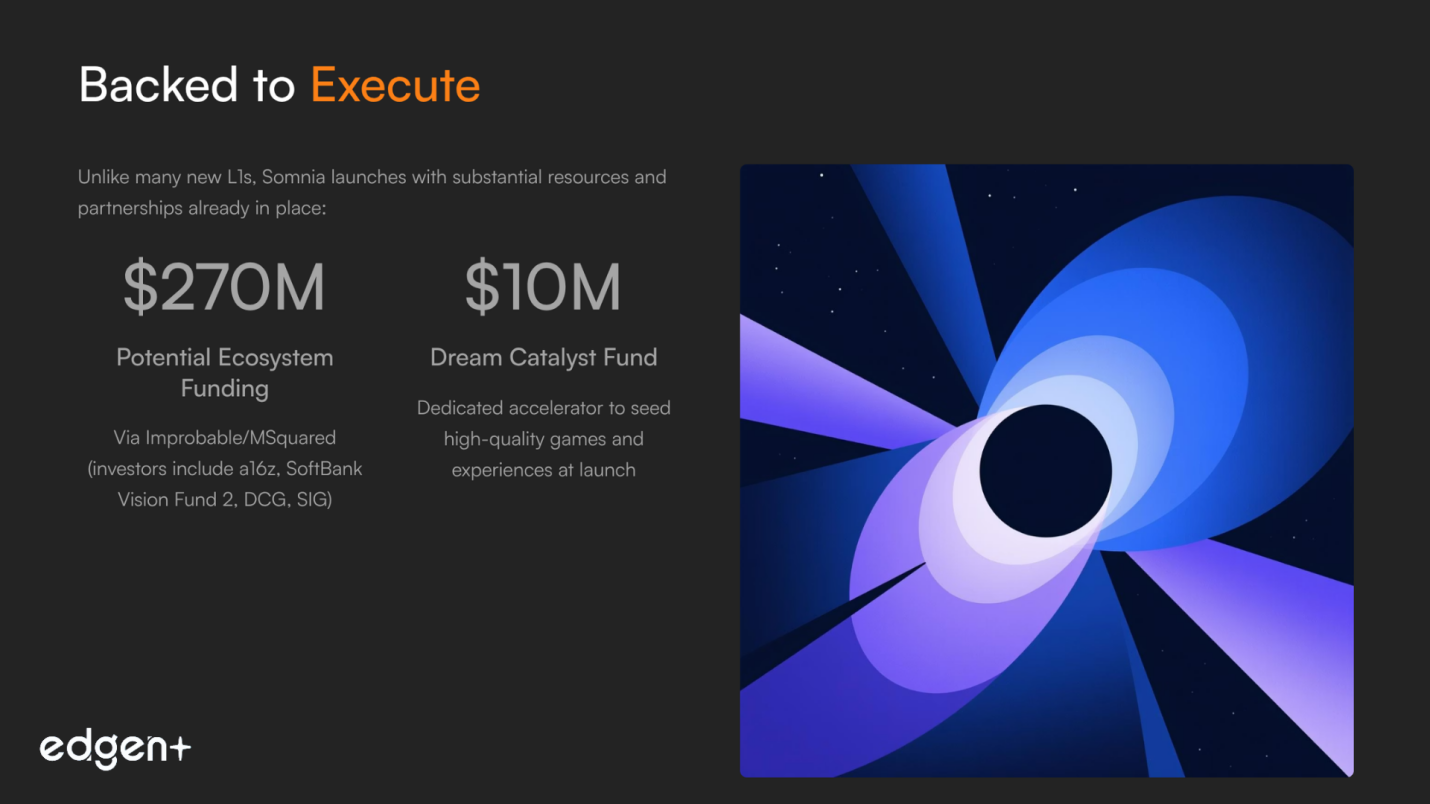

Rather than conventional rounds, Somnia benefits from ecosystem funding up to $270M via Improbable/MSquared (investors include a16z, SoftBank Vision Fund 2, DCG, SIG). Google Cloud validates at an enterprise level (validator + AI/data/security), while Sequence and Rarible accelerate developer and market readiness.

4) Market Opportunity & Fit

On-chain gaming/metaverse is large and expanding. Somnia serves builders who need reliable, high-contention performance with EVM familiarity, plus grants, SDKs, and distribution, reducing both technical and financial switching costs.

5) Competitive Position & Differentiators

Competes with gaming-centric EVM chains (Ronin, Immutable zkEVM, GalaChain) and high-throughput L1s (Solana, Aptos). Differentiation: hot-state execution focus, full EVM, ambitious “Virtual Society” narrative, and authentic virtual-world pedigree from Improbable.

Foundational take: Remarkable foundational strength with aligned capital, credible partners, and a purpose-built design for real-time, on-chain worlds.

II. Pre-Launch Ecosystem & Go-to-Market

1) Community & Narrative Momentum

Top-of-funnel growth is massive, driven by testnet and incentives. The opportunity now is to convert breadth into depth, institutionalize comms, highlight shipped dApps, and channel community energy into mainnet usage.

2) On-Chain Footprint

Testnet activity has been stress-scale, a useful systems proving ground. The key KPI post-TGE is quality usage (DAU, retained wallets, live dApps), not raw transactions.

3) Partnerships & Readiness

- Google Cloud: validator + AI/data/security integration for builders.

- Sequence: smart wallets, Unity/Unreal SDKs, marketplace stack for the Somnia Builder.

- Uprising Labs: $10M Dream Catalyst to seed high-quality games.

Together, these reduce friction from code to users and help ensure day-one content.

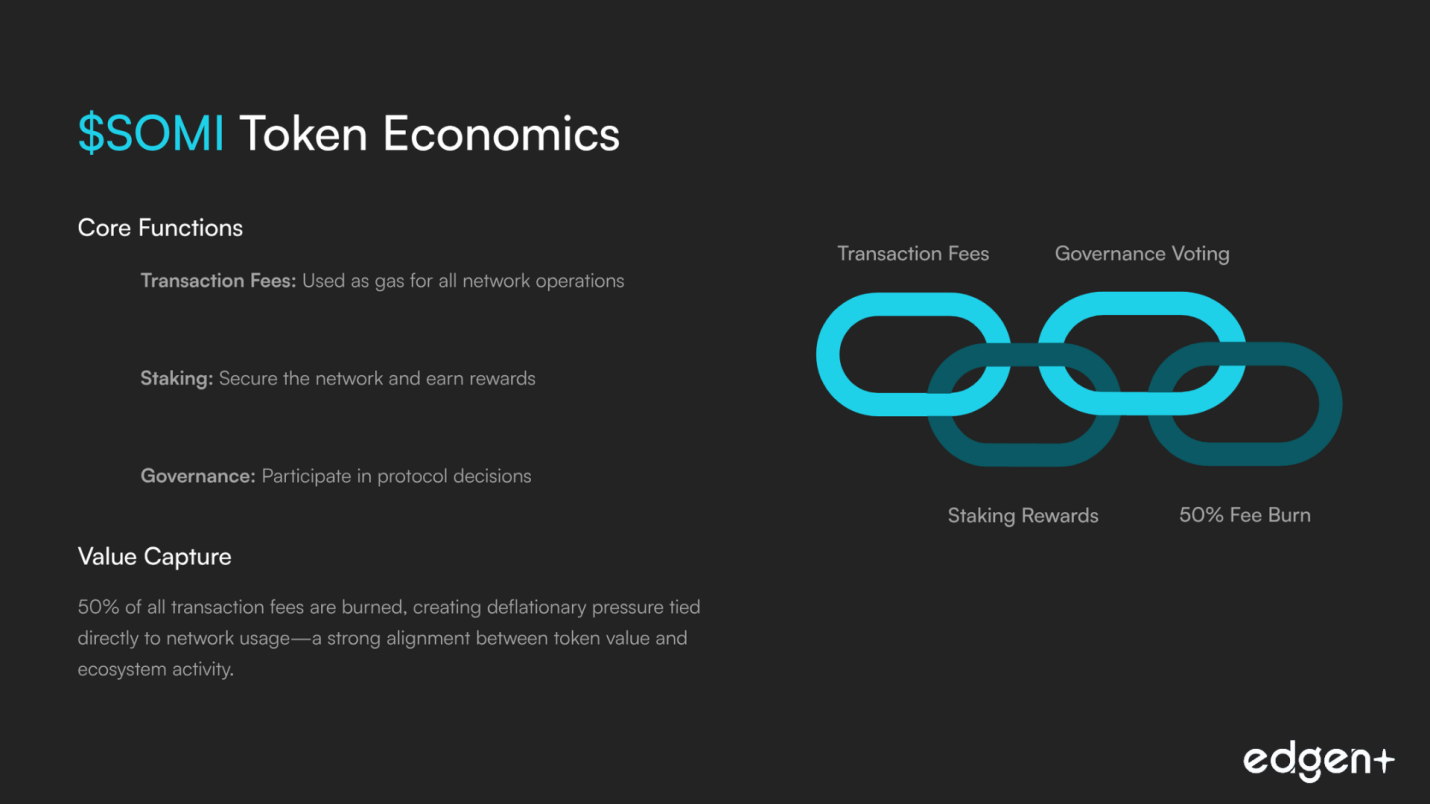

4) Tokenomics & Value Accrual (Today)

$SOMI: gas, staking, governance. 50% fee burn aligns value with usage. Airdrop (5% supply) vests via weekly mainnet quests (20% liquid at TGE; ~80% activity-gated over ~60 days) to encourage real participation from the start.

GTM take: Very promising. The stack, programs, and partners point to strong developer velocity; launch ops (custody/MM/liquidity comms) should be clarified to maximize day-one confidence.

III. Forward-Looking Analysis (Catalysts & Opportunities)

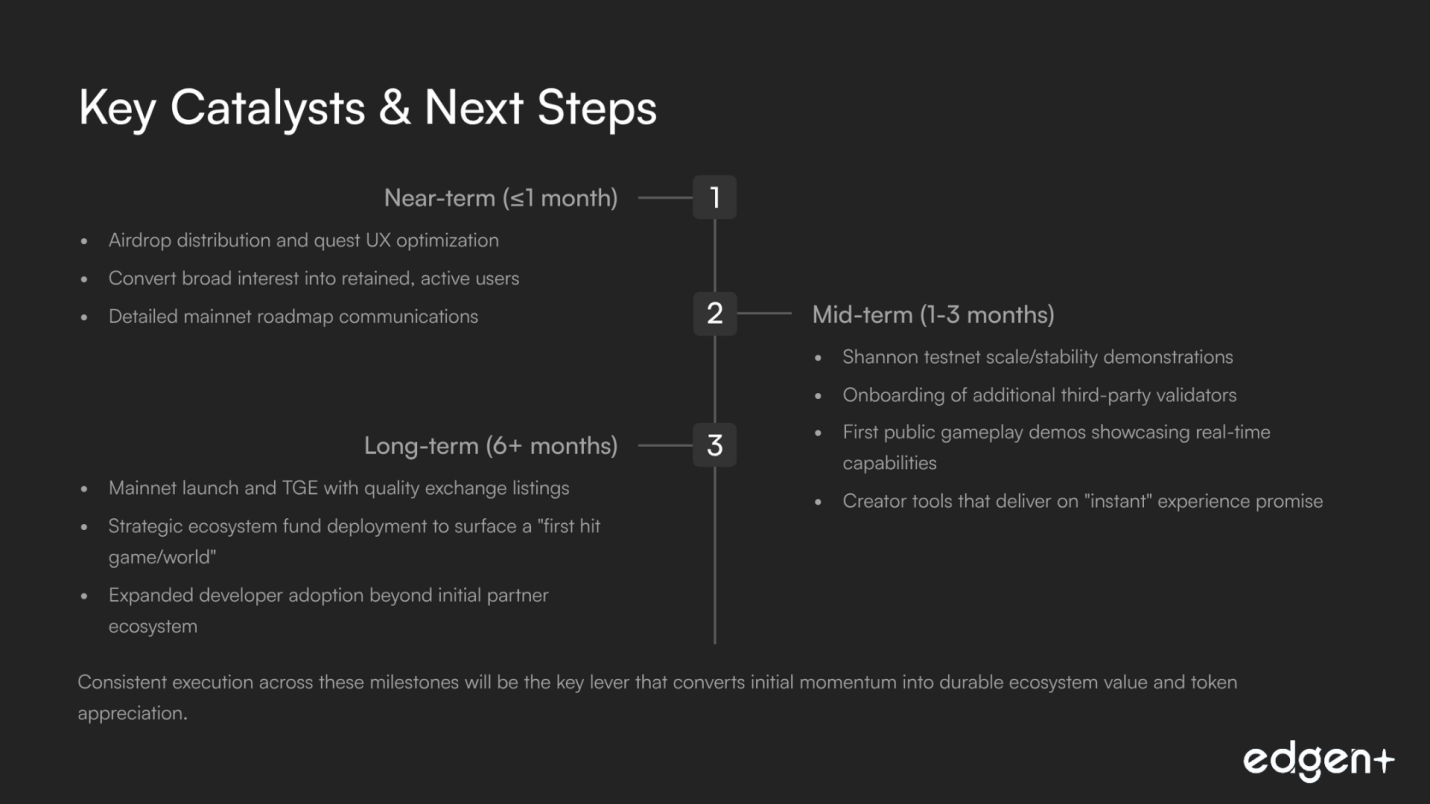

Near-term (≤1 month):

- Communicate airdrop learnings + crystal-clear quest UX. Turning broad interest into happy, retained users can reset sentiment fast.

Mid-term (1–3 months):

- Shannon testnet scale/stability proof and more third-party validators; first public gameplay and creator tools that feel instant.

Long-term (6+ months):

- Mainnet + TGE with quality listings and liquidity; ecosystem fund deployment that surfaces a “first hit game/world.”

Execution cadence is the lever that converts momentum into durable value.

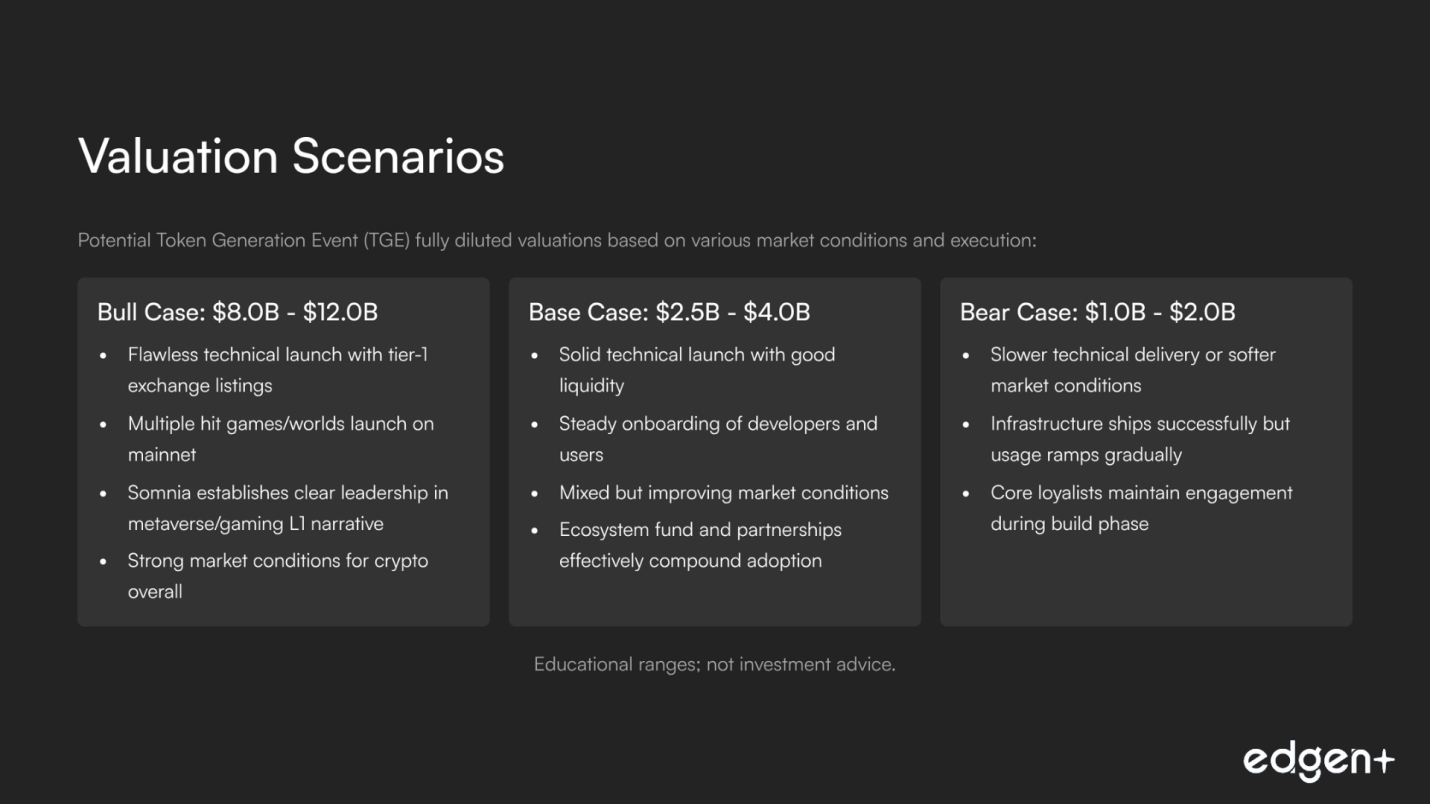

IV. Valuation Scenario Analysis (TGE FDV)

Scenario | FDV (USD billions) | Brief narrative |

Bull Case | 8.0 – 12.0 | Flawless launch + tier-1 listing; hit games go live; Somnia leads metaverse/gaming L1 story. |

Base Case | 2.5 – 4.0 | Solid tech + steady onboarding in a mixed market; fund + partners compound adoption. |

Bear Case | 1.0 – 2.0 | Slower delivery or softer market; infra ships, usage ramps gradually with core loyalists. |

Educational ranges; not investment advice.

Competitor Landscape (token angle at/near TGE)

Network | Token | Focus | Base-Case Position vs Somnia |

Ronin | EVM L1 for gaming (publisher-led) | Strong proven pipeline; Somnia competes on broader open-world scope and raw throughput targets. | |

Immutable zkEVM | $IMX | L2 for games, marketplace strength | Deep studios + infra; Somnia counters with L1 performance + EVM + fee burn. |

Solana | High-throughput L1 (parallel exec) | Mature ecosystem; Somnia differentiates on hot-state performance story and EVM familiarity. | |

Aptos | High-throughput L1 (Move) | Strong tech; Somnia lowers dev friction via EVM + specialized metaverse narrative. |

Final Take

Somnia looks very promising: a specialized, EVM-compatible L1 with a realistic plan to power real-time, on-chain worlds. With significant ecosystem funding, blue-chip partners, and a design aimed squarely at hot-state workloads, it’s set up to translate vision into usage. The path to upper-band valuation is straightforward but strict: crystal-clear launch ops, visible early games, smooth TGE, and consistent shipping.

Educational content; not financial advice.

Your money person, finally.

Try Edgen free. No credit card. No commitment.